Global Robotic Manipulation Market Set to Explode to USD 75.3 Billion by 2032, Propelled by a Monumental 26.2% CAGR as AI Vision and RaaS Disrupt Global Industry

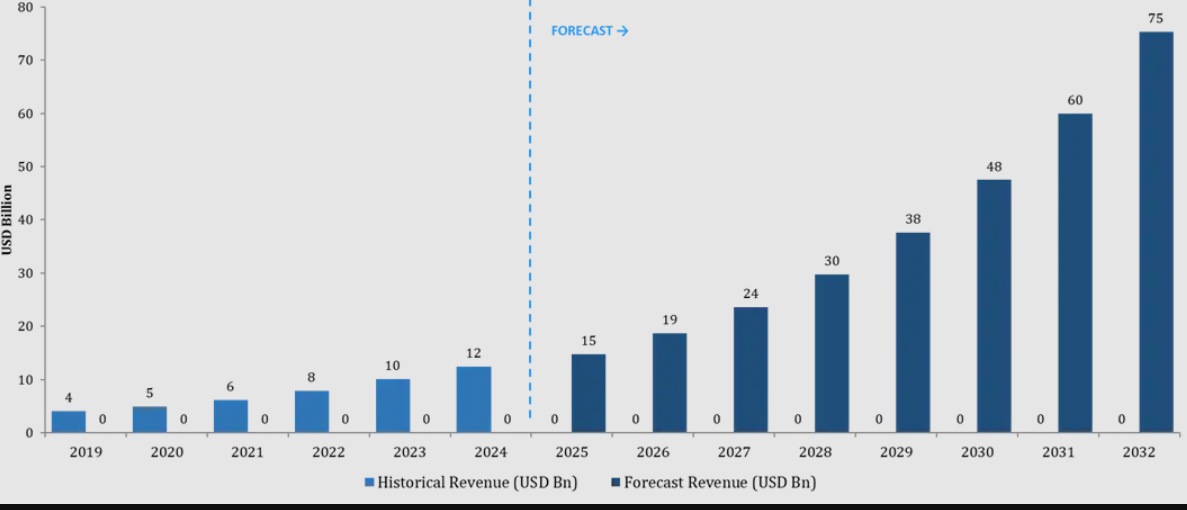

the premier global business intelligence and market research firm, has released a comprehensive, data-driven intelligence report on the Global Robotic Manipulation Market . The extensive study reveals that the market, which was valued at USD 14.8 Billion in 2025 , is on an aggressive multi-year trajectory to reach USD 75.3 Billion by 2032 . This explosive growth represents an outstanding Compound Annual Growth Rate (CAGR) of 26.2% over the forecast period from 2026 to 2032.

The report underscores a profound structural transformation across the industrial landscape: robotic manipulation—defined as the use of programmable mechanical systems to physically interact with, move, assemble, or process objects—is systematically dismantling the final boundary of industrial automation, which is the unstructured environment. Historically constrained to rigid, pre-programmed paths, modern robotic arms equipped with next-generation artificial intelligence (AI) and advanced end-effectors are now adapting to real-time spatial variations, driving unprecedented efficiency gains across manufacturing, e-commerce, logistics, automotive, pharmaceuticals, and consumer goods.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/302259/

Navigating the Unstructured Frontier: The Robotic Shift

According to the Maximize Market Research survey data, a staggering 86% of global industrial companies now plan to deploy robotic manipulation solutions within the next three years. This is a dramatic escalation from the 44% of companies that have active deployments today. This 42-percentage-point adoption gap represents the single largest commercial opportunity in industrial technology over the current decade.

The inflection point in this market is driven by three major converging forces:

-

AI-Powered Vision Systems: Advanced vision algorithms are now achieving a historic 99.7% pick accuracy across completely unstructured bin-picking scenarios, minimizing human intervention.

-

Severe Labor Inflation: Persistent labor shortages and an average 18% increase in manufacturing wages over the past five years have collapsed the traditional Return on Investment (ROI) payback period from 4.2 years down to under 2.3 years.

-

The Collaborative Robot (Cobot) Revolution: Drastic reductions in programming complexity—by up to 60%—have opened a massive USD 3.2 Trillion Small and Medium Enterprise (SME) manufacturing market that was previously completely locked out of traditional robotic automation due to prohibitive costs and technical barriers.

Granular Market Segmentation and Core Structural Dynamics

To provide a clear, panoramic market vision for executive decision-makers, investors, and technology suppliers, the study segments the global robotic manipulation market across five key vectors: Type, Application, Payload capacity, End-User industry, and Geography.

1. By Type: Articulated Robots Lead, While Cobots Experience Hyper-Growth

-

Articulated Robots: This segment continues to hold the lion’s share of the market, accounting for approximately 42% of total market revenue in 2025. Renowned for their multi-axis flexibility, high payload thresholds, and mechanical durability, articulated robotic manipulation arms remain the foundational workhorses of heavy automotive assembly lines, precision welding, and complex machining environments.

-

Collaborative Robots (Cobots): While articulated systems dominate absolute revenue, Cobots represent the fastest-growing segment, expanding at an extraordinary CAGR of 31.4%. Built with integrated force-torque sensors and advanced proximity awareness, cobots eliminate the need for restrictive safety cages, allowing physical collaboration with human workers. This makes them highly attractive for high-mix, low-volume assembly lines and packaging centers.

-

Other Types: This includes Cartesian, SCARA, and parallel/delta robots, which continue to see steady deployment in high-speed, localized pick-and-place electronic assembly and packaging tasks.

2. By Application: Assembly and Logistics Spearhead Adoption

-

Assembly & Disassembly: Complex multi-part assembly processes, especially in the microelectronics and automotive sub-assembly spaces, are driving massive procurement of high-precision robotic manipulation tools.

-

Pick-and-Place & Material Handling: Driven primarily by the warehouse logistics and fulfillment sector, the need to rapidly sort, classify, and transport varying items has elevated pick-and-place applications to a dominant position.

-

Welding, Painting, and Surface Treatment: Highly precise and repeatable manipulation systems reduce material waste and protect human workers from hazardous vapor environments.

3. By Payload Capacity: Diverging Needs for Micro and Macro Automation

-

Low Payload (Below 10 kg): Highly correlated with the rise of cobots and electronics manufacturing, where delicacy, agility, and minimal physical footprint are prioritized.

-

Mid-to-High Payload (10 kg to 100 kg+): Essential for industrial palletizing, heavy parts machining, and structural automotive component positioning.

4. By End-User: Automotive and E-Commerce Generate Continuous Pull

-

Automotive Industry: Historically the primary incubator for industrial robotics, the automotive sector is upgrading legacy lines to handle electric vehicle (EV) battery packs, complex wiring harnesses, and lightweight composite chassis elements.

-

Logistics and E-Commerce: This sector represents the primary engine of market acceleration. The explosive growth of same-day and next-day delivery mandates has outpaced the physical capacity of the human labor pool, requiring autonomous robotic picking at scale.

-

Pharmaceuticals, Food & Beverage, and Electronics: Highly sterile, cleanroom-certified robotic manipulators are scaling rapidly to satisfy rigorous regulatory standards and high-throughput production lines.

Key Drivers Fueling the Market Trajectory

Labor Cost Inflation & ROI Compression

Manufacturing labor costs have escalated sharply on a global scale. Between 2020 and 2025, production worker compensation rose by an average of 18%. For instance, in the United States, production worker wages surged to an average of USD 28.50 per hour in 2025 compared to USD 22.10 in 2019. Conversely, a modern robotic manipulation cell, when properly amortized over a standard 7-year operational lifespan, incurs an equivalent labor expense of just USD 3.80 to USD 6.20 per hour. This massive wage gap makes the financial case for automation undeniable. Payback windows have fallen far below the critical 3-year threshold required by corporate CapEx committees, turning automation into an immediate defensive necessity rather than an optional long-term strategy.

The E-Commerce Volume Paradigm and Warehouse Automation Pull

Global e-commerce transactional volumes expanded by a factor of 3.8x between 2019 and 2025, driven by a structural shift in consumer purchasing habits. With roughly 74% of modern consumers citing rapid fulfillment as a decisive factor in brand loyalty, traditional manual sorting facilities are facing an operational bottleneck. Large-scale deployments, such as Amazon Robotics’ Sparrow system—which processes over 4.5 million individual picks per day across its expansive fulfillment network—have set a new standard for the supply chain sector. This massive infrastructure shift is pulling the entire logistics industry along, with MMR survey metrics indicating that 83% of mid-tier logistics operations are actively scheduling robotic manipulation integration to protect their supply chains against capacity crunches.

Artificial Intelligence, Computer Vision, and Foundation Models

The primary technical barrier to historic robotic deployment was rigidity; robots simply could not handle items that were out of alignment or varied in shape. The incorporation of advanced AI vision systems completely changes this dynamic. Achieving a verified 99.7% pick accuracy in 2024 for highly unstructured bin-picking environments, AI has made autonomous, unsupervised industrial deployment a reality.

Furthermore, the emergence of advanced multimodal foundation AI models (such as GPT-4V and Google DeepMind’s RT-2) has allowed robots to interpret natural language commands and recognize contextual relationships between objects. This reduces the need for expensive, specialized software engineering resources and cuts down initial programming and integration timelines by as much as 60%. Similarly, digital twin technologies enable organizations to completely simulate, stress-test, and refine robotic cells in a virtual sandbox before purchasing physical hardware, slashing on-site commissioning times by 40%.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/302259/

Market Restraints and Challenges to Widespread Integration

Despite the overall positive outlook, the robotic manipulation market faces a few distinct friction points that require strategic navigation:

-

Prohibitive Initial Capital Expenditure (CapEx): A fully engineered, integrated, and safety-certified robotic manipulation cell typically commands an upfront price tag ranging from USD 200,000 to USD 800,000 depending on payload and vision complexity. This upfront capital allocation creates a significant balance sheet constraint for smaller enterprises.

-

Integration Complexity with Legacy Operations: Interfacing cutting-edge robotic controllers with decades-old Programmable Logic Controllers (PLCs), Enterprise Resource Planning (ERP) systems, and Manufacturing Execution Systems (MES) results in an industry-average deployment window of 14 months, placing temporary strains on internal operational technology (OT) teams.

-

The Global Robotics Talent Deficit: According to data from the International Federation of Robotics (IFR), the global economy is tracking toward a deficit of 2.4 million unfilled specialized robotics and automation engineering roles by 2030. Enterprises frequently find themselves capable of financing hardware but fundamentally constrained by an inability to recruit internal talent to operate, optimize, and maintain these sophisticated systems.

The RaaS (Robotics-as-a-Service) Revolution

To break down the steep upfront CapEx barrier and address the ongoing talent shortage, the industry is witnessing a massive pivot toward the Robotics-as-a-Service (RaaS) subscription framework. RaaS bundles physical robotic hardware, proprietary AI vision software, cloud-linked operational updates, and full preventative maintenance into a predictable, operationalized monthly subscription fee.

The RaaS market segment is currently expanding at an extraordinary 38% CAGR. Pioneering providers like Formic Technologies and Rapid Robotics are deploying pick-and-place automation setups at operational price points as low as USD 5.50 per hour. By positioning automated labor as a direct, variable OpEx cost that undercuts human wage structures without requiring any upfront capital allocation, RaaS allows small-to-medium manufacturers to achieve immediate cost savings. Maximize Market Research forecasts that the RaaS model will capture an impressive 22% of total global robotic manipulation market revenue by 2032, up from a modest 4% share recorded in 2025.

Regional Industry Forecast: North America Leads, Asia-Pacific Accelerates

North America (Market Share Dominance)

North America maintained its position as the leading geography, commanding approximately 35% of global market revenue in 2025. The region’s dominance is anchored by rapid warehouse automation deployments across major logistics corridors, massive corporate investment in AI software, and an aggressive push by the automotive and aerospace industries to reshore manufacturing capabilities.

Asia-Pacific (Fastest-Growing Region)

The Asia-Pacific marketplace is projected to register the most rapid growth through 2032, expanding at an exceptional CAGR of 28.1%. This economic acceleration is underpinned by massive government-backed factory modernization programs across India, China, and Southeast Asia. India’s manufacturing ecosystem alone is injecting over USD 68 Billion into comprehensive industrial automation through 2030, positioning robotic manipulation at the core of its expanding electronics assembly, electric vehicle, and pharmaceutical supply chains.

Europe (Regulatory and Sustainability Champion)

Europe continues to exhibit steady, robust demand for advanced robotic manipulation, heavily driven by stringent workplace safety regulations and ambitious green manufacturing goals. The European market prioritizes high-efficiency collaborative robot arrays and advanced end-effectors capable of minimizing material waste and energy consumption across the automotive and chemical processing landscapes.

Value Chain Dynamics and the Margin Shift

An analytical assessment of the robotic manipulation value chain reveals an important economic truth: profit pools are shifting away from basic structural hardware toward software intelligence layers.

While raw materials and sub-system hardware manufacturing (servo motors, structural steel casting) operate on tight gross margins of 6% to 14%, the specialized Software & AI Layer enjoys commanding gross margins ranging from 28% to 40%. As specialized AI firms continue to scale, the industry's center of gravity is shifting from traditional hardware manufacturing to intelligence platforms. This structural change mirrors the automotive industry’s transition toward software-defined vehicles, where long-term value is unlocked by advanced software capabilities rather than standard mechanical assembly.

+---------------------------------------------------------------------------------+

| ROBOTIC MANIPULATION VALUE CHAIN |

+---------------------------------------------------------------------------------+

| 1. Component Supply --> 2. OEM Assembly --> 3. Software/AI --> 4. End-User|

| (6% - 14% Margin) (25% - 35% Margin) (28% - 40% Margin) Deployment |

+---------------------------------------------------------------------------------+

| *Value is shifting rapidly from physical assembly to the AI intelligence layer.*|

+---------------------------------------------------------------------------------+

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/robotic-manipulation-market/302259/

Competitive Landscape and Market Intel

The global robotic manipulation market features a highly consolidated core of established industrial giants, complemented by a fast-growing ecosystem of agile AI startups and cobot specialists. Key market players detailed in the report include:

-

FANUC Corporation (Japan)

-

ABB Robotics (Switzerland)

-

KUKA AG (Germany)

-

Yaskawa Electric Corporation (Japan)

-

Universal Robots A/S (Denmark)

-

Kawasaki Heavy Industries, Ltd. (Japan)

-

Nachi-Fujikoshi Corp. (Japan)

-

Stäubli International AG (Switzerland)

-

Comau S.p.A. (Italy)

-

Denso Wave Incorporated (Japan)

- Franka Emika (Agile Robots)(Germany)

- RealTime Robotics(USA)

To maintain their competitive edge, these industry incumbents are actively forming strategic partnerships with or acquiring mid-tier AI vision startups. This allows them to deliver pre-configured, out-of-the-box autonomous picking cells that reduce system integration friction. Concurrently, regional players in China and South Korea are introducing cost-disruptive entry-level collaborative platforms, putting pressure on hardware margins and accelerating adoption across cost-sensitive business segments.

Strategic Vision and Executive Action: Driving Effective Corporate Decisions

For executive leadership teams, the findings of this report highlight an important truth: automation is no longer an optional tool for driving incremental efficiency; it has become an essential strategy for long-term operational resilience. Organizations that delay their automation plans run the risk of falling behind competitors that operate with significantly lower variable labor costs and around-the-clock operational capacities.

Executive Recommendation Framework

-

Transition to OpEx Models: Corporate CFOs should actively evaluate RaaS options to bypass traditional CapEx restrictions, allowing immediate operational deployment while preserving valuable cash reserves.

-

Prioritize Modular Software Platforms: Avoid vendor lock-in by investing in open-architecture robotic systems that integrate easily with third-party AI vision upgrades, advanced end-effectors, and ROS2-compliant management software.

-

Upskill the Workforce Internally: Address the global engineering talent deficit by executing internal training initiatives, transforming traditional line operators into certified managers of automated robotic cells.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656