Global Chromatography Reagents Market Projected to Reach USD 18.21 Billion by 2032, Anchored by 11.04% CAGR as Biologics R&D and Ultra-Purity Mandates Fuel Demand

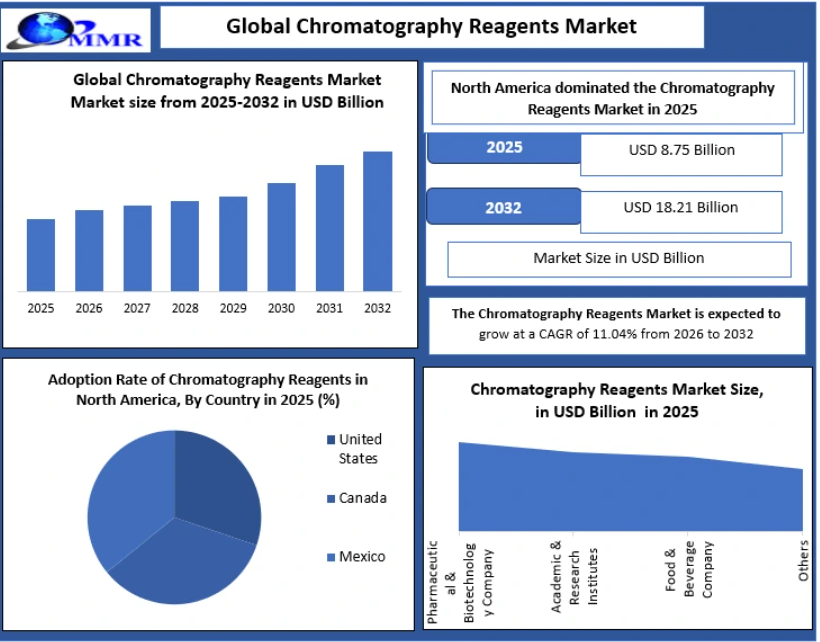

a leading global business intelligence and chemical sector consulting firm, has released its exhaustive, data-verified intelligence report on the Global Chromatography Reagents Market. The comprehensive study reveals that the market, valued at USD 8.75 Billion in 2025, is on an aggressive multi-year trajectory to reach USD 18.21 Billion by 2032. This robust expansion represents an exceptional Compound Annual Growth Rate (CAGR) of 11.04% over the forecast period from 2026 to 2032.

The report highlights a significant structural shift within analytical testing laboratories: the demand for chromatography reagents is no longer driven by routine laboratory volume updates. Instead, it is fueled by a structural expansion in global pharmaceutical R&D pipelines, tightening environmental regulations, and the rapid growth of the biologics and biosimilars sector. These factors have turned high-purity solvents, buffers, and ion-pair reagents into critical assets for maintaining precise analytical workflows across High-Performance Liquid Chromatography (HPLC), Gas Chromatography (GC), and Liquid Chromatography-Mass Spectrometry (LC-MS) platforms.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/302291/

Precision in Analytics: The Drivers of Chromatography Reagent Acceleration

According to Maximize Market Research analytical models, analytical testing requirements across the healthcare, environmental compliance, and food safety sectors have increased significantly. As global regulatory bodies like the US FDA and the European Medicines Agency (EMA) enforce lower detection limits for impurities and genotoxic genotoxicants, the requirement for ultra-pure, batch-consistent chromatography reagents has transitioned from a premium preference to an absolute operational necessity.

The current market expansion is driven by three major converging forces:

-

The Biosimilar and Biologics Surge: The global shift toward complex large-molecule therapeutics requires advanced bio-chromatography separation and purification workflows, multiplying the volume of specialty reagents required per analytical run.

-

Strict Environmental and PFAS Infrastructure Testing: Heightened regulatory monitoring of forever chemicals, microplastics, and pesticide runoff has caused double-digit increases in routine testing frequencies at contract research and municipal testing facilities.

-

Massive Adoption of High-Sensitivity LC-MS Systems: The rapid migration from traditional detectors to ultra-sensitive mass spectrometry instruments has accelerated the demand for specialized LC-MS grade solvents, which minimize background noise and prevent instrument contamination.

Granular Market Segmentation and Strategic Industry Matrix

To provide corporate strategists, laboratory groups, and chemical manufacturers with a clear market vision, the study segments the global chromatography reagents market across four primary operational areas: Reagent Type, Separation Method, End-User Industry, and Geography.

1. By Reagent Type: High-Purity Solvents Command Major Volume and Value

-

Chromatography Solvents: This segment continues to hold the largest market share, accounting for over 55% of global market revenue in 2025. Solvents such as acetonitrile, methanol, water, and acetone serve as the foundational mobile phase components across nearly all automated separation workflows. The segment is experiencing clear premiumization, with demand shifting rapidly from standard gradient grade to specialized LC-MS and UHPLC ultra-purity grades.

-

Buffers and Mobile Phase Modifiers: Essential for maintaining stable pH environments during complex protein and small-molecule separations. This segment is growing steadily, driven by the expanding biopharmaceutical sector.

-

Ion-Pair Reagents and Derivatization Agents: These specialty categories are registering high growth due to their ability to enhance the volatility or selectivity of highly polar compounds during specialized gas and liquid chromatography separations.

-

Stationary Phase Modifiers: Includes specialized surface silanization agents and surface modification compounds that optimize column chemistry performance.

2. By Separation Method: Liquid Chromatography (HPLC/UHPLC) Monopolizes Reagent Pull

-

Liquid Chromatography (LC/HPLC/UHPLC): This method dominates reagent consumption globally. Liquid chromatography systems require a continuous flow of high-purity mobile phases, making them the primary volume engine for solvent and buffer suppliers.

-

Gas Chromatography (GC): Remains a vital analytical methodology for volatile organic compounds (VOCs), petrochemical analysis, and environmental screening, maintaining a stable and predictable demand footprint for high-purity organic solvents.

-

Ion Chromatography and Supercritical Fluid Chromatography (SFC): Represent niche, high-growth technical segments that require highly specialized mobile phase combinations and high-purity carbon dioxide modifiers.

3. By End-User Industry: Pharmaceuticals and Biopharma Spearhead Consumption

-

Pharmaceutical & Biotechnology Companies: Representing the largest absolute consumption vertical, this sector drives over 45% of total market value. Reagents are integrated across the entire drug life cycle, from early-stage discovery and high-throughput screening to process scale-up, validation, and commercial batch quality control.

-

Environmental Testing Laboratories: A fast-growing customer segment driven by expanding governmental legislation monitoring drinking water safety, soil toxicity, and industrial air emissions.

-

Food and Beverage Safety: Driven by global export compliance requirements, food testing laboratories utilize intensive chromatography assays to detect residual veterinary drugs, heavy metals, and adulterants.

-

Academic and Government Research Institutes: Maintaining continuous, baseline consumption profiles linked to public healthcare research grants and baseline synthetic chemistry research programs.

Key Technical and Economic Dynamics Shaping the Industry

The Economics of Regulatory Compliance and Impurity Profiling

The primary economic driver for premium reagent consumption is the increasing risk of product recalls and regulatory friction in the pharmaceutical space. Under current ICH (International Council for Harmonisation) guidelines, impurity profiles must be validated down to trace levels. Using inferior or inconsistent reagents can cause artifact peaks, baseline drift, and column deterioration.

A single contaminated analytical batch or a false positive reading can halt commercial pharmaceutical packaging lines, costing an organization between USD 150,000 and USD 500,000 per day in operational downtime. To protect validation processes, corporate procurement teams are establishing long-term, single-source contract frameworks with Tier-1 organized reagent producers who can guarantee rigorous lot-to-lot traceability and complete chemical certification.

Feedstock Price Volatility and Supply Chain Optimization

The chromatography reagents market faces notable operational challenges due to raw material volatility. The synthesis and purification of core solvents like acetonitrile—frequently generated as a byproduct of acrylonitrile manufacturing—are directly exposed to disruptions in global petrochemical production. Price fluctuations in crude chemical intermediates can erode margins for chemical processors.

To mitigate these supply chain risks, laboratory networks and major contract testing organizations are shifting from spot-market ordering toward structured, multi-year volume supply agreements. Concurrently, top-tier reagent manufacturers are optimizing their supply chains by expanding local distribution hubs and offering bulk automated solvent delivery systems to minimize packaging waste and reduce total logistical expenses.

+---------------------------------------------------------------------------------+

| ROUTINE CHROMATOGRAPHY WORKFLOW & TIMELINE |

+---------------------------------------------------------------------------------+

| 1. Discovery R&D --> 2. Process Development --> 3. Commercial QC Testing |

| (High-Purity Solvents) (Method Optimization) (Trace Impurity Profiling) |

+---------------------------------------------------------------------------------+

| *Reagent consistency across all three stages is vital to avoid validation failures.*|

+---------------------------------------------------------------------------------+

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @:https://www.maximizemarketresearch.com/request-sample/302291/

Regional Industry Projections: North America Leads, Emerging Markets Accelerate

North America (The Value and Infrastructure Hub)

North America maintained its position as the leading regional market, commanding a prominent share of global chromatography reagents revenue in 2025. The region's position is supported by the world's largest pharmaceutical R&D investment base, high HPLC and LC-MS adoption rates, and a dense network of contract research organizations (CROs). Stringent environmental testing mandates across municipal wastewater systems further accelerate baseline solvent and buffer consumption across the United States and Canada.

Asia-Pacific (The High-Velocity Growth Engine)

The Asia-Pacific marketplace is projected to expand at the fastest pace through 2032, driven by a rapid shift in pharmaceutical manufacturing and active pharmaceutical ingredient (API) processing toward India and China. India’s active expansion in generic drug manufacturing, combined with China's government-backed biotechnology initiatives, has created a massive volume pull for analytical reagents. Local producers in these regions are also scaling their distillation capabilities to meet international regulatory standards, capitalizing on competitive regional pricing models.

Europe (The Hub for Strict Quality Standardization)

The European marketplace continues to exhibit steady, resilient demand for chromatography reagents, heavily driven by the strict implementation of European Pharmacopoeia and environmental compliance directives. The European market prioritizes green chemistry initiatives, which is encouraging chemical suppliers to develop eco-friendly solvent alternatives and sustainable recycling programs for large-scale industrial preparative chromatography processes.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/chromatography-reagents-market/302291/

Competitive Intensity Mapping and Market Structure

The global chromatography reagents market features a dual structure: a consolidated core of international chemical and life science corporations controls roughly 65% of global revenue, while regional, unorganized suppliers compete primarily on price in less-regulated application areas.

Featured Industry Leaders Profiled in the Report:

-

Thermo Fisher Scientific Inc. (United States)

-

Merck KGaA / Sigma-Aldrich (Germany)

-

Agilent Technologies, Inc. (United States)

-

Waters Corporation (United States)

-

Avantor, Inc. (United States)

-

Honeywell International Inc. (United States)

-

Bio-Rad Laboratories, Inc. (United States)

-

Shimadzu Corporation (Japan)

-

FUJIFILM Wako Pure Chemical Corporation (Japan)

-

TCI Chemicals (Tokyo Chemical Industry Co., Ltd.) (Japan)

To maintain long-term customer relationships, major market players are focusing heavily on digital integration. By embedding automated inventory replenishment software directly within a laboratory's procurement platform, reagent suppliers can automatically track usage patterns and ship replacement lots before a facility experiences an inventory shortage. This closed-loop software ecosystem helps lock in long-term account value and creates high switching barriers for competing commodity suppliers.

Value Chain Dynamics: Strategic Profit Pool Allocation

An analytical assessment of the chromatography reagents value chain highlights that economic value is concentrated within specialized purification and certification phases rather than basic chemical synthesis.

+---------------------------------------------------------------------------------+

| CHROMATOGRAPHY REAGENTS VALUE CHAIN MAP |

+---------------------------------------------------------------------------------+

| Raw Petrochemical Feedstock -> Advanced Multistage Distillation -> Analytical Validation |

| (Commodity / Low Margin) (Highly Specialized Operations) (Premium Margin) |

+---------------------------------------------------------------------------------+

| *The highest margins belong to suppliers offering verified batch-to-batch trace consistency.*|

+---------------------------------------------------------------------------------+

While basic raw chemical manufacturing operates on thin commodity margins, advanced multi-stage fractional distillation and analytical validation steps capture premium margins. Companies that invest in high-end analytical testing infrastructure to certify their lots for specialized applications, such as UHPLC and mass spectrometry, can achieve significant margin advantages over suppliers of standard industrial-grade solvents.

Tactical Framework for Corporate Laboratory Decisions

For laboratory directors, pharmaceutical procurement managers, and clinical research executives, the evolving chromatography reagents market requires a structured approach to asset management:

-

Prioritize Batch-to-Batch Consistency: Procurement strategies should prioritize long-term batch consistency over short-term price variations. Minimizing chromatographic baseline drift helps reduce instrument downtime and prevents costly method re-validation cycles.

-

Mitigate Acetonitrile Supply Risks: Given the historical volatility of the acetonitrile supply chain, laboratory managers should evaluate dual-sourcing strategies or validate alternative methanol-based mobile phase methodologies where appropriate.

-

Incorporate Automated Replenishment Systems: Transition analytical facilities toward IoT-enabled smart storage networks that monitor reagent consumption in real time, preventing inventory shortages and minimizing internal warehousing overhead.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize market Reserach

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656