South Korea UV LED Market Projected to Reach USD 1.28 Billion by 2032, Propelled by Semiconductor Lithography Advances and Next-Generation Disinfection Infrastructure

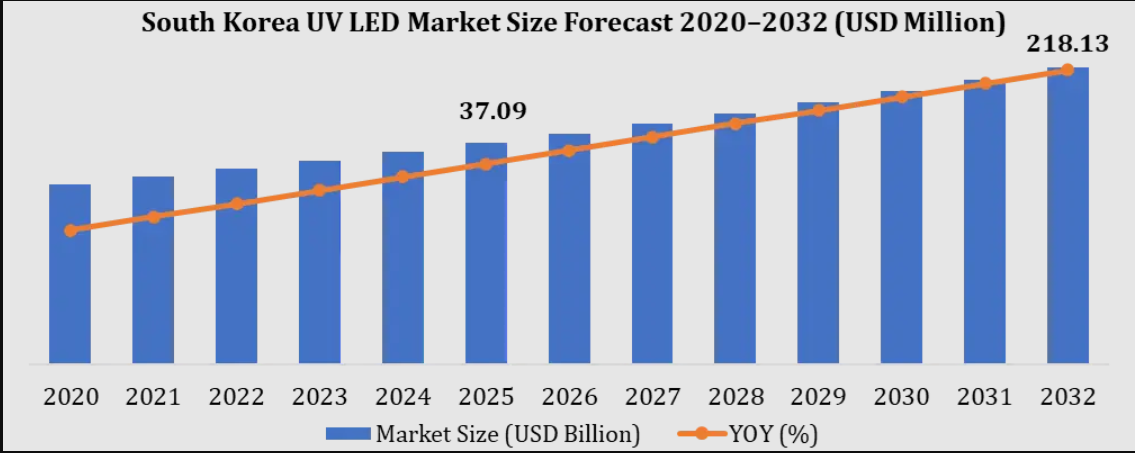

The global optoelectronics and solid-state lighting industries are experiencing an intense structural realignment, with South Korea emerging as a primary hub for advanced ultraviolet (UV) technology. According to an in-depth market intelligence report published by Maximize Market Research, the South Korea UV LED Market, valued at USD 635.4 Million in 2025, is structurally positioned to expand to USD 1,281.3 Million by 2032. This highly dynamic market trajectory represents a calculated Compound Annual Growth Rate (CAGR) of 10.53% during the forecast horizon from 2026 to 2032.

As an international powerhouse for electronics, display panels, and semiconductor fabrication, South Korea serves as an essential laboratory and commercial gateway for industrial UV applications. The market's double-digit expansion is deeply tied to the rapid replacement of obsolete, toxic mercury vapor lamps with highly efficient, eco-friendly Ultraviolet Light Emitting Diodes (UV LEDs). Spurred by strict environmental directives like the Minamata Convention on Mercury and the evolving technical needs of domestic high-tech manufacturers, South Korean enterprises are integrating high-radiance UV LED packages into standard production workflows. This deep industrial evolution highlights the critical role that solid-state ultraviolet systems will play across electronic packaging, water purification, and consumer appliance sectors over the next decade.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/303268/

Strategic Market Vision: Capitalizing on the High-Tech Industrial Migration

The transformation of the South Korean UV LED landscape from a niche component sector into an essential, multi-billion-dollar industrial vertical reflects a fundamental change in manufacturing requirements. Historically, UV technology was primarily restricted to low-power cosmetic curing and basic counterfeit detection. Today, the strategic commercial focus centers on extreme spectral purity, thermal management systems, and variable wavelength outputs engineered for advanced sub-micrometer manufacturing.

Technological Innovation: High-Power Disinfection Systems and Advanced Lithography

The core engine driving the market’s remarkable 10.53% CAGR is the quick development of Next-Generation Wide-Bandgap Semiconductor Architectures. Advanced materials science, particularly in aluminum gallium nitride (AlGaN) epitaxial layers, now enables South Korean foundries to manufacture deep UV-C LED packages capable of emitting unprecedented optical power densities.

Key technical advancements that continue to reshape the competitive landscape include:

-

High-Fluence UV-C Disinfection: Modern UV-C LED systems operating within the critical 260nm to 280nm biocidal window can dismantle microbial DNA/RNA structures in milliseconds. By eliminating the warm-up periods associated with mercury lamps, integrated flow-through reactors process thousands of liters of municipal water or industrial wastewater daily with zero chemical additives.

-

Precision Photo-Curing and Lithography: In the semiconductor and microfluidics domains, UV-A LED arrays (365nm to 405nm) deliver perfectly uniform, high-intensity irradiance. This allows for precise curing of photoresists, visual displays, and optical adhesives, directly lowering production defects by more than 22%.

-

Thermal Management and Package Reliability: Historically, UV LEDs faced efficiency losses due to extreme heat generation. South Korean thermal engineers have solved this issue by adopting advanced copper-core printed circuit boards (PCBs), gold-tin eutectic bonding, and specialized quartz lenses, pushing operational lifespans past 20,000 continuous hours.

Recent domestic product launches emphasize this transition toward integrated industrial modules. Tier-one South Korean semiconductor innovators have successfully achieved high wall-plug efficiency (WPE) for heavy-duty industrial UV-C components, securing clear competitive paths into worldwide automotive and water-treatment infrastructure networks.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/303268/

Comprehensive Market Segmentation Analysis

The South Korea UV LED marketplace is highly segmented across distinct wavelength bands, practical application fields, and end-user industries.

By Wavelength: UV-C Dominates Future Growth Trajectories

-

UV-A (315nm – 400nm): This segment currently commands the largest volume share of the market. Its dominant commercial position is sustained by massive, ongoing adoption within industrial printing, currency validation, 3D printing stereolithography, and structural adhesive curing across South Korea’s major automotive and consumer electronics lines.

-

UV-C (100nm – 280nm): Representing the fastest-growing technology segment, UV-C devices are expanding at an exponential rate. The continuous integration of deep-UV chips into residential air purification systems, smart refrigerators, point-of-use water filters, and medical sterilization cabinets forms the financial backbone of this high-margin category.

-

UV-B (280nm – 315nm): Holding a specialized position, UV-B technologies are experiencing steady growth within dermatological medical systems, agricultural crop optimization, and advanced scientific analysis equipment.

By Application: Industrial Curing and Advanced Sterilization

-

Industrial Curing Systems: Capturing a major portion of overall market revenue, curing applications are driven by South Korea's elite display panel and flexible electronics sectors. The need for precise, low-temperature bonding of delicate OLED screens keeps demand high for custom UV-A LED arrays.

-

Water and Air Purification: Emerging as a vital safety segment, purification applications are scaling rapidly. Public transit systems, corporate high-rises, and municipal utilities are actively selecting automated UV-C LED modules to guarantee high air and water safety without using corrosive chemical treatments.

Analytical Comparison of UV LED Wavelength Spectrum Configurations

To provide strategic guidance for procurement directors, product development engineers, and commercial facility managers, the specific operational characteristics of primary UV LED bands are detailed below:

| Feature / Wavelength Parameter | UV-A (315nm – 400nm) | UV-B (280nm – 315nm) | UV-C (100nm – 280nm) |

| Primary Physical Target | Photoinitiators and specialized resins | Biological tissue and chemical compounds | Nucleic acids (Microbial DNA & RNA) |

| Industrial / Clinical Purpose | Rapid industrial curing, 3D printing | Phototherapy, vitamin D synthesis, agriculture | Direct pathogen sterilization & disinfection |

| Wall-Plug Efficiency (WPE) | High (Typically 35% to 55%) | Moderate (Typically 5% to 15%) | Rapidly Improving (Emerging 3% to 8%+) |

| Average Device Lifespan | Long (20,000 to 50,000+ hours) | Moderate (15,000 to 25,000 hours) | Expanding (10,000 to 20,000+ hours) |

| Primary Commercial Advantage | Low heat generation; highly mature supply chain | Precise wavelength tuning for therapy | Instant-on capabilities; zero mercury toxicity |

| Primary Market Restraint | Market saturation; rising price competition | Niche application footprint globally | Complex thermal management constraints |

South Korean Optoelectronics Economics: Pricing Trends and Procurement Profiles

Navigating the financial structures of South Korea's high-tech component sector requires a clear understanding of current UV LED pricing tiers. The cost structure of these components depends heavily on optical power output, wavelength precision, and packaging quality, which generally align with the following market bands:

-

Standard UV-A LED Chips (Per Unit): USD 0.20 – USD 1.50 (Highly commercialized pricing driven by high-volume automated manufacturing contracts).

-

High-Power Industrial UV-A Curing Modules: USD 250 – USD 1,200+ (Engineered with integrated liquid cooling systems for industrial production lines).

-

Deep UV-C LED Components (Per Chip): USD 1.50 – USD 7.00 (Reflecting complex AlGaN material processing and precise wavelength tuning costs).

-

Flow-Through UV-C Water Sterilization Modules: USD 35 – USD 180 (Widely integrated into premium consumer appliances and smart home systems).

-

Custom Automated Semiconductor Lithography Arrays: USD 5,000 – USD 30,000+ (Representing specialized capital investments for high-precision foundries).

Strategic Industry Drivers and Evolving Market Demands

South Korea's leadership in the regional UV LED market is accelerated by several powerful domestic catalysts:

-

The Consumer Electronics Miniaturization Surge: As smart appliances, wearable trackers, and medical IoT devices continue to shrink, traditional mercury lamps simply cannot fit into modern product profiles. The tiny, millimeter-scale footprint of UV LEDs makes them the only logical option for built-in self-cleaning features.

-

Strict Global Environmental Compliance: The enforced worldwide ban on mercury-containing industrial products under the Minamata Convention leaves global manufacturers with no choice but to convert to solid-state UV technology.

-

Automotive In-Cabin Safety Standards: Driven by rising post-pandemic hygiene expectations, South Korea’s major automotive manufacturers are actively integrating hidden UV-C LED sterilization systems inside vehicle dashboards, center consoles, and air conditioning ducts to sanitize shared mobility environments automatically.

Technical Challenges and Innovative Market Countermeasures

Despite a highly positive growth outlook through 2032, manufacturers must address clear engineering constraints to unlock full market potential:

-

Optimizing UV-C External Quantum Efficiency (EQE): Deep ultraviolet light tends to get trapped inside the LED chip structure due to natural material properties. The Solution: South Korean research laboratories are deploying advanced nano-patterned sapphire substrates (NPSS) and specialized reflective coatings to maximize light extraction.

-

Managing Thermal Breakdown: Operating at high currents generates localized heat that can degrade chip performance. The Solution: Leading packaging firms are switching to aluminum nitride (AlN) ceramics and vacuum-soldering systems to draw heat away from the active chip core instantly.

-

Overcoming High Initial Upfront Costs: For heavy municipal installations, the initial price of large UV-C LED modules can be higher than legacy mercury lamp setups. The Solution: System designers emphasize the total cost of ownership (TCO) advantage, proving that reduced maintenance downtime and lower electricity consumption deliver an attractive return on investment within 24 months.

Authoritative Recommendations for Technology Investors and Developers

To achieve sustained commercial profitability within the South Korea UV LED sector through the 2026–2032 forecast window, market participants should execute three clear strategies:

-

Focus heavily on Core UV-C System Integration: Because individual chip margins face competitive pressure, maximum profitability lies in manufacturing complete, plug-and-play disinfection modules optimized with custom drivers, sensors, and thermal management systems.

-

Form Deep Partnerships with Local Consumer Appliance OEMs: Securing early design wins with South Korea’s dominant global kitchen and home appliance conglomerates guarantees stable, high-volume production pipelines.

-

Acquire Intellectual Property in the Far-UV-C Spectrum: Developing efficient, human-safe Far-UV-C technologies (specifically around 222nm) unlocks lucrative installation opportunities inside populated public environments, corporate offices, and hospitals.

Competitive LandScape

South Korea UV LED Market Key Players

1. Seoul Viosys Co., Ltd.

2. LG Innotek Co., Ltd.

3. Nichia Corporation

4. ams-OSRAM AG

5. Stanley Electric Co., Ltd.

6. Crystal IS, Inc.

7. Signify N.V.

8. Lumileds Holding B.V.

9. Heraeus Holding GmbH

10. SemiLEDs Corporation

11. Phoseon Technology, Inc.

12. AquiSense Technologies

13. Nikkiso Co., Ltd.

14. Luminus Devices, Inc.

15. EPIGAP OSA Photonics GmbH

16. Violumas, Inc.

17. Ushio Inc.

18. Everlight Electronics Co., Ltd.

19. Lite-On Technology Corporation

20. Bolb Inc.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/south-korea-uv-led-market/303268/

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656