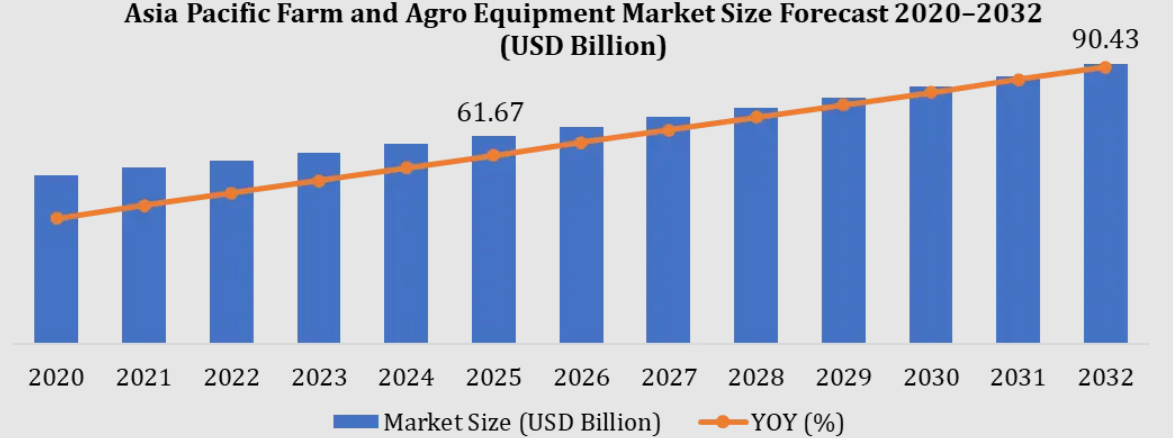

Asia-Pacific Farm and Agro Equipment Market Driven by Smart Mechanization and Precision Agriculture to Advance Rural Productivity

A leading global business intelligence and strategic consulting firm, has released its highly anticipated comprehensive market study titled "Asia-Pacific Farm and Agro Equipment Market Industry Analysis, Trends, and Forecast (2026–2032)". The extensive research report highlights a defining paradigm shift sweeping across the agricultural landscape of the Asia-Pacific (APAC) region. Driven by shrinking rural labor pools, structural government subsidies, and the urgent demand for optimized crop yields, the APAC Farm and Agro Equipment Market is poised to achieve unprecedented scale, reinforcing its position as a global cornerstone of agricultural technological adoption.

As the region transitions from traditional, labor-intensive farming methods to institutionalized, tech-driven practices, capital investment in mechanized equipment is climbing significantly. Large-scale public initiatives—ranging from agricultural credit extensions in India to massive rural modernization mandates in China and Southeast Asia—are actively encouraging the adoption of advanced tractors, smart harvesters, automated irrigation infrastructures, and UAV (unmanned aerial vehicle) crop protection systems.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/305803/

Navigating the Macroeconomic Transition: The Strategic Imperatives of APAC Mechanization

For decades, agriculture across the Asia-Pacific territory was categorized by fragmented landholdings and an abundance of low-cost manual labor. However, structural demographic transitions are reshaping this model. Rapid urbanization has drawn younger generations away from traditional farming, triggering acute seasonal labor shortages and driving up operational wages for farm operators.

Consequently, farm mechanization has transformed from a long-term capital choice into an immediate operational necessity. The regional push toward high-efficiency agricultural machinery ensures that sowing, cultivation, and harvesting cycles remain tightly optimized, shielding food supply networks from sudden demographic gaps. Furthermore, because climate variability creates unpredictable monsoon and rain patterns across the APAC region, the adoption of speed-efficient machinery allows corporate agribusinesses and smallholder cooperatives to complete intensive field preparation cycles in a fraction of historical timelines.

Core Market Drivers: Precision Farming, Drone Integration, and Financial Stimulus

The structural expansion of the Asia-Pacific farm and agro equipment landscape is underpinned by several powerful structural catalysts:

-

Escalating Adoption of Precision Agriculture: Farmers are increasingly adopting data-driven solutions, including GPS-guided tractors, IoT-enabled soil monitoring systems, and automated seed-drilling equipment. These technologies mitigate input waste by applying exact volumes of seeds, water, and fertilizers, protecting thin profit margins against rising chemical costs.

-

The Rapid Integration of Agricultural Drones: Drone technology is experiencing a massive surge across the APAC region, particularly in China, Japan, and India. Utilized primarily for targeted crop protection, aerial imaging, and ultra-precise pesticide spraying, agricultural drones minimize direct chemical exposure for operators while covering expansive acreage with unmatched speed.

-

Targeted Government Subsidies and Credit Schemes: Public financial support remains one of the most powerful catalysts for equipment deployment in developing APAC sub-markets. Programs such as India’s Sub-Mission on Agricultural Mechanization (SMAM) and matching-grant subsidies across ASEAN nations drastically reduce the initial capital expenditure barrier for smallholder farming groups, enabling them to transition from handheld tools to high-horsepower mechanical assets.

Segment Analysis: Tractors Maintain Dominance While Smart Harvesting Solutions Accelerate

To deliver comprehensive clarity for C-suite decision-makers and institutional investors, the report segments the Asia-Pacific market across several critical vectors: by Equipment Type, Technology, Application, and End-User Framework.

Tractors Form the Bedrock of Regional Sales

Tractors continue to capture the largest volume share of the APAC farm equipment sector. This enduring dominance is sustained by their extensive, multi-functional utility. Modern mid-to-high-horsepower tractors function as foundational mechanical platforms, capable of powering attached implements for plowing, land development, sowing, structural crop protection, and heavy-duty rural logistics. To cater to the region's diverse topographies—ranging from massive open wheat fields in Northern China to dense, waterlogged paddy fields in Southeast Asia—leading manufacturers are diversifying their portfolios, offering both compact utility tractors for small-scale operations and heavy-duty, automated options for large-scale corporate farms.

Harvesting and Threshing Machinery Gain Rapid Momentum

As post-harvest crop loss remains a critical challenge to food security across developing economies, the demand for combined harvesters and multi-crop threshing machinery is expanding rapidly. These integrated systems accelerate harvesting windows, protecting mature crops from sudden unseasonal weather events while optimizing structural grain separation quality. This segment is experiencing notable technical integration, with manufacturers adding digital grain-loss sensors and real-time yield monitoring software directly into harvester cabins.

Technology Bifurcation: The Convergence of Conventional and Smart Machinery

While conventional, high-durability mechanical equipment retains a substantial volume share due to its affordability and straightforward maintenance profile among small-scale farms, the smart farming segment is registering the highest growth rate. Driven by a regional push toward eco-efficient operations, the market is seeing a steady increase in zero-emission electric machinery, smart autonomous implements, and data-connected fleet tracking technologies that allow agribusiness managers to monitor asset utilization from centralized mobile applications.

Critical Regional Insights: Profiling the Key Growth Engines of APAC

China: The Manufacturing Heavyweight and Automation Pioneer

China stands out as both a massive consumer base and a major manufacturing hub for agricultural machinery within the region. Supported by explicit state mandates aimed at ensuring comprehensive grain self-sufficiency and deep rural revitalization, Chinese agricultural operators are rapidly integrating advanced automation. The domestic market is characterized by large-scale deployments of automated, driverless tractors guided by domestic BeiDou satellite navigation networks, transforming the country's northern and western agricultural provinces into highly automated production zones.

India: A Powerhouse Driven by Subsidies and Custom Hiring Centers (CHCs)

India represents one of the largest global markets for tractor volumes. The structural growth of the Indian market is tightly linked to aggressive mechanization policies and the strategic rise of Custom Hiring Centers (CHCs). Because individual smallholders often face capital constraints preventing direct ownership of high-tier machinery, CHCs function as equipment-rental networks. This decentralized model allows small-scale farmers to access high-performance harvesters, laser land levelers, and power tillers on a flexible pay-per-use basis, democratizing technology access across rural states.

Southeast Asia and Australasia: Diverse Landscapes, Specialized Demands

The ASEAN sub-market, led by Thailand, Vietnam, and Indonesia, exhibits a growing demand for specialized, lightweight machinery engineered for wet-rice cultivation and dense plantation management. Conversely, the Australasian sector (Australia and New Zealand) mirrors Western operational scales, with a highly commercialized agribusiness sector focused on large-scale, high-horsepower machinery, precision pasture management tools, and advanced telematics for extensive livestock and grain operations.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/305803/

Supply Chain Realities and Strategic Industry Challenges

Despite structural growth indicators, international and regional equipment manufacturers must successfully navigate distinct systemic challenges to protect long-term profitability:

-

High Initial Capital Costs and Financing Barriers: Advanced, precision-enabled machinery requires substantial initial capital outlays. In developing economic corridors where rural banking penetration can be inconsistent, securing flexible, low-interest asset financing remains a primary hurdle for small-scale farming associations.

-

Fragmented Landholdings Resisting Large-Scale Implements: A significant portion of the arable land across nations like India, Bangladesh, and Vietnam consists of small, disconnected plots. This fragmentation limits the physical operational efficiency of expansive, high-horsepower combined machinery, forcing engineering teams to redesign products into smaller, highly maneuverable configurations.

-

Logistical Vulnerabilities and Component Cost Volatilities: The agricultural machinery supply chain remains vulnerable to global commodity price fluctuations, particularly for high-grade structural steel, cast components, and semiconductor chips essential for smart navigation control panels. Manufacturers are increasingly focused on building localized supply chains to buffer operations against cross-border transport disruptions and currency fluctuations.

Intense Competitive Dynamics and Strategic Corporate Movements

The Asia-Pacific Farm and Agro Equipment Market features a highly competitive blend of established global manufacturing conglomerates and fast-growing domestic brands utilizing cost-effective production models to gain regional market share.

Leading enterprise organizations profiled within this extensive market intelligence study include:

-

Deere & Company

-

Kubota Corporation

-

Mahindra & Mahindra Ltd.

-

AGCO Corporation

-

CNH Industrial N.V.

-

Yanmar Co., Ltd.

-

CLAAS KGaA mbH

-

SDF Group

-

Escorts Kubota Limited

-

TAFE (Tractors and Farm Equipment Limited)

- Mitsubishi Mahindra Agricultural Machinery

. Buhler Industries

Corporate engineering and market penetration strategies are increasingly centered around building strategic local joint ventures, establishing regional assembly hubs to optimize import tariff exposure, and introducing specialized, robust product lineups tailored specifically to regional soil conditions and crop profiles.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/apac-farm-and-agro-equipment-market/305803/

Strategic Action Plan for Agribusiness Executives and Global Investors

To capitalize on the high-velocity modernization of Asia-Pacific agriculture, enterprise leaders and financial allocators should adopt a focused, three-pronged strategy:

-

Develop Scalable Micro-Mechanization Portfolios: Product engineering should focus heavily on "micro-mechanization"—creating compact, highly versatile, and fuel-efficient power units that offer precision capabilities like GPS tracking and automated seeding, but are scaled specifically for small and medium-sized fields.

-

Form Strategic Partnerships with Rental and Custom Hiring Networks: Rather than relying entirely on traditional dealer-to-owner retail structures, global brands can drive consistent volume by directly partnering with state-backed equipment rental agencies and independent Custom Hiring Centers. This approach unlocks immediate volume sales while building long-term brand equity across fragmented farming demographics.

-

Integrate Localized Telematics and Robust Support Networks: To secure long-term brand loyalty, machinery must be backed by accessible, regional maintenance ecosystems and simple, language-localized digital interfaces. Providing field-level mechanics with comprehensive training and ensuring rapid, regional spare-parts availability functions as a critical competitive differentiator in high-intensity farming belts.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656