Global Camera Market Valuation to Reach USD 23.76 Billion by 2032, Driven by Mirrorless Ecosystems, AI Integration, and Content Creation Boom

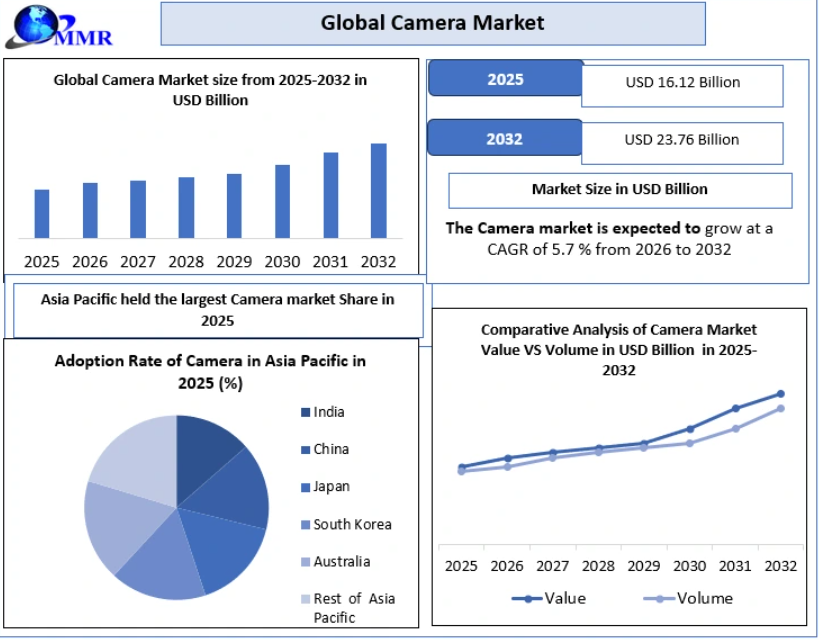

the Global Camera Market was valued at USD 16.12 Billion in 2025 and is mathematically projected to scale to USD 23.76 Billion by 2032. This reflects a compound annual growth rate (CAGR) of 5.7% during the forecast window spanning 2026 to 2032.

The industry’s expansion is heavily fueled by a structural pivot from traditional DSLR infrastructure toward mirrorless systems, the democratization of high-tier video production tools for digital content creators, and aggressive integration of edge-computed artificial intelligence within consumer, security, and industrial imaging ecosystems.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/304127/

Executive Market Overview & High-Level Architecture

The structural mechanics of the modern camera market are no longer confined to recreational or classical studio photography. Today, the sector stands at a critical intersection of computational hardware, machine learning firmware, and optoelectronic engineering. As social platforms and commercial digital media demand professional-grade spatial resolution and advanced color science, the hardware ecosystem has responded with highly adaptive, compact, and interconnected imaging nodes.

Historically, Digital Single-Lens Reflex (DSLR) architectures dominated the professional market via mechanical mirror assemblies and optical viewfinders. However, contemporary data gathered across global manufacturing supply chains indicates that the market has definitively crossed its inflection point. Electronic viewfinders (EVFs), reduced flange focal distances, and the superior continuous autofocus capabilities of mirrorless systems are capturing the primary market share.

Furthermore, industrial, automotive, security, and healthcare applications are establishing massive baseline demand, transforming the camera market into a highly diversified b2b and b2c conglomerate.

Key Market Metrics & Statistical Framework

The underlying data models utilized for this evaluation isolate key performance indicators across historical and predictive timelines:

-

Base Year Baseline: USD 16.12 Billion (2025)

-

Forecasted Terminal Value: USD 23.76 Billion (2032)

-

Compounded Growth Rate: 5.7% CAGR (Allocated 2026–2032)

-

Historical Data Architecture: 2020 to 2025

-

Leading Structural Dynamic: Rapid adoption of mirrorless form factors over legacy DSLR systems.

-

Primary Regional Value Capture: Asia Pacific (holding dominant market share driven by infrastructural investments and centralized manufacturing).

Core Drivers Transforming the Global Camera Landscape

1. The Mirrorless and Hybrid Imaging Paradigm Shift

The relentless migration of consumer and commercial capital into mirrorless systems is the most visible driver in the hardware sector. By eliminating the mechanical mirror box, manufacturers have not only optimized the physical footprint and durability of cameras but have opened the door to faster burst tracking and zero-blackout continuous shooting. Hybrid imaging—the engineering paradigm where a single sensor performs equally well at high-bitrate video capture and raw still output—has expanded the addressable market to include videographers, independent cinema houses, and mixed-media organizations.

2. Exponential Growth of Content Creation and Social Platforms

The rise of digital content generation across diverse streaming environments has altered consumer expectations. Independent creators, vloggers, and corporate digital marketing departments are consistently scaling their technical setups. Standard smartphone optics, while highly optimized via software, frequently hit optical limits regarding depth of field, low-light performance, and lens modularity. This has driven a substantial wave of secondary purchases targeting mirrorless bodies, advanced action cameras, and specialized multi-directional 360-degree systems.

3. Artificial Intelligence Integration and Edge Computational Photography

The embedding of deep-learning algorithms within camera processors has unlocked tracking matrices that were previously impossible. Modern image processors now utilize real-time subject recognition systems capable of identifying and maintaining absolute focus on human eyes, animal profiles, high-speed motor vehicles, and avian trajectories. Beyond focus acquisition, AI algorithms running directly on the camera hardware optimize dynamic range, reduce thermal noise profiles at elevated ISO settings, and streamline on-the-fly digital stabilization.

In-Depth Market Segmentation Analysis

The global camera market is analyzed by segmenting its structural variables across product classifications, technologies, connectivity protocols, end-use applications, and distribution pathways.

Analysis by Product Type

-

Mirrorless Cameras: This segment represents the highest concentration of research and development expenditure and capital deployment. It commands the highest average selling prices (ASPs) among interchangeable lens systems.

-

DSLR Cameras: While losing ground in terms of new manufacturing unit volume, the DSLR segment maintains a notable operational footprint among legacy users, educational systems, and specialized studio environments that prioritize battery longevity and optical workflows.

-

Action and 360-Degree Cameras: Driven by rugged sports, adventure tourism, and immersive virtual reality production, these ultra-compact devices are sustaining independent growth paths, particularly within younger consumer cohorts.

-

Point-and-Shoot: Standard compact digital cameras have largely been absorbed by mobile phone capability. However, a premium sub-tier—featuring large 1-inch sensors and fast fixed prime lenses—has emerged as a highly profitable lifestyle and street photography niche.

Analysis by End-User Vertical

-

Consumer Electronics & Media: Captures the highest percentage of total consumer-facing revenue. The rapid monetization of individual digital channels ensures a constant refresh cycle for optical hardware.

-

Security & Surveillance: High-resolution optical arrays combined with thermal and night-vision capabilities are experiencing massive adoption across smart-city developments and commercial real estate assets.

-

Healthcare & Scientific Research: High-speed, high-sensitivity imaging systems are vital nodes within microscopy, non-invasive diagnostic surgical devices, and advanced laboratory observation.

Regional Landscape & Strategic Imperatives

Asia Pacific: The Global Nexus of Production and Consumption

The Asia Pacific geographic zone maintains undisputed leadership in the camera market. This dominance is dual-pronged, structural, and cultural. On the supply side, the vast majority of premium optical foundries, sensor manufacturing cleanrooms, and assembly infrastructures are physically located across Japan, China, Taiwan, South Korea, and Thailand.

On the demand side, the rapid economic expansion of regional superpowers, coupled with rising disposable incomes and an expansive demographic of young, tech-native digital media producers, ensures consistent domestic market absorption.

North America & Europe: Centers for Enterprise and Advanced Workflows

The Western markets exhibit mature, high-value consumption patterns. In North America, the entertainment capital concentration drives extensive procurement of cinematic and ultra-high-resolution (4K/8K UHD) systems.

Concurrently, European regulatory environments regarding public safety and automation have accelerated deployment of advanced intelligent camera architectures within automated manufacturing plants, logistics centers, and traffic safety infrastructure.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/304127/

Competitive Landscape & Market Consolidation Matrices

The global camera domain is highly consolidated, characterized by intense technological rivalries among a select cohort of long-standing legacy engineering organizations. These industry participants are protecting their market share by developing enclosed ecosystem dynamics—specifically proprietary lens mount systems that create long-term consumer retention.

The primary market participants evaluated in the comprehensive report include:

1. Canon Inc.

2. Nikon Corporation

3. Sony Group Corporation

4. Fujifilm Holdings Corporation

5. Panasonic Corporation

6. OM Digital Solutions Corporation

7. Olympus Corporation

8. Leica Camera AG

9. Sigma Corporation

10. GoPro

11. Pentax

12. Hasselblad

13. Phase One

14. DJI

15. Samsung Electronics

16. Huawei

17. Blackmagic Design

18. RED Digital Cinema

19. Arri

20. JVC

21. Kodak

22. Ricoh

23. Zeiss

24. Casio

25. Acer

26. Toshiba

27. Sharp

28. Benq

29. Vivitar

Corporate strategy among these players has shifted away from volume-driven price wars toward value-driven innovation. Manufacturers are deliberately targeting the higher-margin professional and semi-professional ("prosumer") categories to offset the loss of low-end consumer volume to modern mobile device platforms.

Strategic Market Challenges and Growth Restraints

Despite the robust upward trajectory of the macro market value, several key bottlenecks require active mitigation by enterprise stakeholders:

1. High Capital Requirements for Premium Equipment

The developmental costs associated with advanced full-frame sensors and complex lens element configurations mean premium systems remain financially out of reach for broad amateur demographics. This high cost of entry can limit immediate consumer adoption rates, pushing entry-level users to rely on high-end smartphones instead of transitioning to dedicated cameras.

2. Accelerated Obsolescence Cycles

The velocity of computational updates and sensor iteration shortens product cycles. For corporate buyers, camera rental firms, and professional production studios, this rapid shift presents a clear amortization challenge. Investing heavily in a fleet of devices that may face technical obsolescence within a 36-month window requires precise asset management.

3. Raw Material Volatility and Semiconductor Constraints

Premium optics rely on specific rare-earth elements for specialized glass casting, alongside highly sophisticated microprocessors. Geopolitical changes, supply chain disruptions, and shifting international trade policies can instantly impact production costs, margins, and global delivery timelines.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/camera-market/304127/

Corporate Actions & Actionable Insights for Investors

This business intelligence report serves as a primary tool for investment allocations, resource planning, and long-term product roadmapping. Organizations seeking to preserve market share or successfully enter the optical space must emphasize the following strategic points:

-

Prioritize Open System Interoperability: Software APIs and cloud-integrated video-to-cloud workflows are becoming just as critical to the purchasing decision as raw sensor megapixel counts.

-

Invest in Specialized Optoelectronics: Expanding product lines into non-consumer spaces—such as industrial automation cameras, machine vision nodes, and medical endoscope imaging—offers resilient, high-margin revenue streams that balance consumer retail fluctuations.

-

Incorporate Subscription Software Architecture: Bridging hardware sales with software-as-a-service (SaaS) elements, including cloud storage solutions, advanced LUT/color profiling processing platforms, and AI-assisted automated editing tools, creates stable recurring revenue models.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656