APAC Robotic Manipulation Market Poised for Exponential Growth, Driven by Industry 4.0 Proliferation and AI-Driven Smart Factory Ecosystems

A premier global business intelligence and market consulting firm, has released its highly anticipated and exhaustive study on the Asia-Pacific (APAC) Robotic Manipulation Market. The comprehensive industry report offers an in-depth, multi-dimensional analysis of the modern automation ecosystem, mapping out key growth drivers, technological transitions, structural market impediments, and competitive matrices.

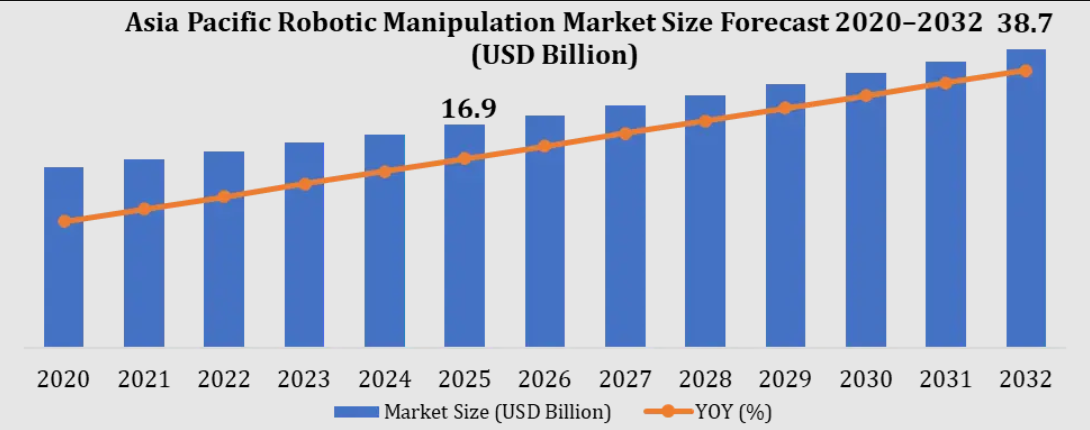

According to the publication, the APAC robotic manipulation sector is undergoing a massive paradigm shift. Driven by structural shifts in labor availability, accelerating industrialization across emerging territories, and the massive integration of Next-Gen artificial intelligence (AI) and machine vision, the market size is tracking toward unprecedented milestones. The market analysis reveals that the continuous convergence of operational technology (OT) with advanced information technology (IT) has positioned the APAC region as the primary growth engine for global industrial automation, capturing more than half of the total global incremental expansion.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/306253/

Executive Summary: Mapping the Next Era of Industrial Autonomy

The competitive landscape of manufacturing has evolved beyond simple mechanization. Today, robotic manipulation—encompassing highly sophisticated multi-axis articulated arms, selective compliance assembly robot arms (SCARA), delta architectures, and advanced collaborative robots (cobots)—is the baseline requirement for maintaining global supply chain resilience.

The APAC region is historically and strategically positioned as the manufacturing hub of the world. However, rising cost pressures, structural labor deficits in highly industrialized states like Japan and South Korea, and a collective regional mandate for hyper-precision have collectively driven a surge in the acquisition of advanced manipulators.

The new report segments the market comprehensively by component (hardware, software, and integration services), by payload capacities (under 16 kg, 16–60 kg, 60–225 kg, and heavy payloads exceeding 225 kg), by application (material handling, assembly/disassembly, welding, processing, and cleanroom sorting), and by key end-user industries (automotive, electrical & electronics, pharmaceuticals, food & beverage, and e-commerce logistics).

Core Market Dynamics and Macroeconomic Growth Triggers

To understand why the APAC robotic manipulation market is exhibiting a double-digit compound annual growth rate (CAGR), forward-thinking enterprises must look at the underlying macroeconomic factors forcing this shift.

1. Structural Labor Deficits and Demographic Trajectories

Several dominant economies across the Asia-Pacific region are confronting significant demographic bottlenecks. Japan and South Korea are dealing with historically low birth rates and rapidly aging workforces. This demographic inversion creates an immediate deficit in skilled and manual floor labor. Automated robotic manipulation systems fill this widening vacuum. Instead of merely substituting workers, these systems allow existing personnel to move into higher-level supervisory, analytical, and maintenance tracks, optimizing human capital efficiency.

2. The Rise of Agentic AI and Intelligent Vision Systems

Legacy robotic arms operated on rigid, deterministic code—they could only pick up an object if it was placed in an exact, predefined spatial position. The modern APAC robotic manipulation market is defined by the integration of vision-language-action (VLA) models and decentralized edge processing. Equipped with highly sophisticated 3D vision systems and machine learning algorithms, modern robotic manipulators can accurately sort mixed, unstructured parts from a random bin, adapt to variations in real-time payload textures, and dynamically adjust path planning to avoid human operators.

3. E-commerce Boom and High-Throughput Intralogistics

The retail landscape across APAC has fundamentally shifted, led by exponential growth in domestic e-commerce across India, China, and Southeast Asian nations. High-throughput fulfillment operations demand rapid order processing with near-zero margins for error. Robotic manipulators integrated with Autonomous Mobile Robots (AMRs) are increasingly used for picking, sorting, split-case packing, and robotic palletization. This seamless orchestration of mobile platforms and stationary manipulation mechanisms has transformed conventional warehouses into agile, dark-store fulfillment assets.

Segment Analysis: Identifying High-Alpha Investment Channels

A granular examination of the market reveals specific sub-sectors that present the highest ROI potential for technology developers, component suppliers, and industrial venture capitalists.

Hardware Dominance with Software as the Core Value Accelerator

While robust mechanical components—such as harmonic drive gearboxes, precision servo motors, and structural chassis—account for the largest nominal share of capital expenditure, the software and programming segment is projected to register the fastest growth rate. The value allocation within the robotics value chain is decisively shifting toward intelligent orchestration layers. Fleets of multi-axis arms now require cloud-connected middleware, predictive maintenance analytics, and standardized application programming interfaces (APIs) to ensure multi-vendor interoperability. Platforms utilizing Robot Operating System (ROS-based) industrial environments are seeing rapid enterprise deployment.

The Explosion of the Collaborative Robotics (Cobot) Frontier

Historically, industrial manipulators were restricted to heavy, isolated safety cages due to high kinetic forces and lack of sensory awareness. The collaborative robot segment is breaking down these physical barriers. Engineered with high-resolution torque sensors, tactile skins, and power/force limiting safety architectures, cobots work directly alongside human teams. This segment is growing rapidly among small and medium-sized enterprises (SMEs) across APAC because it requires far less floor space and features dramatically lower integration and custom-tooling costs compared to traditional high-payload automated setups.

Regional Footprint: China, Japan, India, and South Korea Lead the Charge

The geographic landscape of the APAC robotic manipulation market is diverse, characterized by different manufacturing maturities, localized policy frameworks, and investment capacities.

China: The World's High-Velocity Automation Hub

China stands as the single largest deployment base and geographic hub within the APAC market. Driven by the national "14th Five-Year Robotics Plan," the country combines massive industrial scale with deep localized manufacturing clusters. Domestic Chinese component suppliers have aggressively localized production, dropping the total cost of installation and making multi-axis robotic manipulation accessible to mid-market electronics and general manufacturing firms. The massive electric vehicle (EV) battery production ecosystems inside China serve as a primary user of advanced heavy-payload manipulators.

Japan: The Automation Exporter and Pioneer

Japan represents a mature, highly sophisticated robotics market. It acts as both a primary consumer of precision manipulation and the world's leading exporter of advanced industrial systems. Japanese engineering powerhouses have consistently set the global baseline for reliability and component longevity. The domestic focus in Japan has heavily shifted toward high-dexterity micro-assembly manipulation to serve the ultra-precise semiconductor packaging and advanced medical device industries.

India: The Fastest-Growing Automation Frontier

India is emerging as the fastest-growing market for robotic manipulation in the APAC region. Fueled by national manufacturing initiatives like "Make in India" and substantial production-linked incentive (PLI) schemes, multinational corporations are establishing advanced manufacturing footprints across the Indian subcontinent. While automotive assembly lines have historically used the vast majority of Indian industrial robots, sectors like pharmaceuticals, packaging, and FMCG (Fast-Moving Consumer Goods) are scaling up automated systems to meet both growing domestic demand and strict international quality compliance standards.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/306253/

Strategic Implementation Roadmap for Enterprise Decision-Makers

Deploying an industrial robotic manipulation network requires a strategic approach that goes beyond simply purchasing hardware off the shelf. Organizations looking to integrate automation into their existing operations must focus on long-term scalability and business readiness.

Industry Bottlenecks: Overcoming Integration and Interoperability Hurdles

Despite the clear economic advantages, deployment rates face specific headwind factors that developers and end-users must strategically manage.

The Challenge of High Initial Capital Expenditure and Custom Tooling

For many mid-market enterprises and SMEs across developing Asian economies, upfront acquisition and integration costs remain a significant hurdle. While the price of standard robotic arms has consistently decreased over the past decade, the custom engineering required to design specialized End-of-Arm Tooling (EoAT), custom safety shielding, and bespoke programmable logic controller (PLC) programming can double the initial budget. To combat this, innovative pricing strategies like Robotics-as-a-Service (RaaS) are gaining initial traction, allowing companies to transition high capital expenditure (CapEx) investments into predictable operating expenses (OpEx).

Legacy Infrastructure and System Interoperability

Most brownfield manufacturing facilities operate on a complex mix of legacy machinery, proprietary communication protocols, and disjointed software platforms. Integrating a modern, AI-enabled robotic manipulator into an outdated factory floor often creates data bottlenecks and operational friction. Achieving true synchronization between a new robotic controller, an older conveyor system, and a facility's overarching Manufacturing Execution System (MES) demands deep domain expertise and adherence to open communication standards like OPC Unified Architecture (OPC UA).

Competitive Intelligence: Key Vendors and Strategic Maneuvers

The APAC robotic manipulation market features a highly competitive landscape with consolidated market power among established global leaders, alongside an active tier of agile, specialized regional providers. Dominant market participants highlighted in the comprehensive report include :-

1. ABB Ltd.

2. FANUC Corporation

3. Yaskawa Electric Corporation

4. KUKA AG

5. Mitsubishi Electric Corporation

6. Kawasaki Heavy Industries

7. Omron Corporation

8. Universal Robots

9. Nachi-Fujikoshi Corporation

10. Epson Robots

11. Denso Corporation

12. Staubli Robotics

13. Siemens AG

14. Bosch Rexroth

15. Toshiba Machine

16. Hyundai Robotics

17. Techman Robot

18. Doosan Robotics

19. Yamaha Robotics

20. Rockwell Automation

The primary competitive strategies used by these leaders center around massive investments in research and development (R&D). Top-tier vendors are focusing on developing high-durability, energy-efficient architectures that lower the overall cost of ownership. Strategic partnerships between robotic hardware OEMs and software developers are also increasing, aimed at delivering pre-configured, out-of-the-box automation solutions tailored to specific industries. This minimizes onsite deployment timelines and simplifies the integration process for end-users.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/apac-robotic-manipulation-market/306253/

Forward Outlook: Driving a High-Performance Automation Vision

Looking toward the end of the decade, the APAC robotic manipulation market is positioned to move past isolated, task-specific applications. The future of manufacturing lies in the realization of fully orchestrated, autonomous factory ecosystems. As 5G industrial networks deploy across major manufacturing zones, they will unlock ultra-low latency wireless control channels, allowing centralized AI engines to direct fleets of adaptive manipulators in real time.

For corporate executives, operations directors, and investment planners, the transition to advanced robotic manipulation is no longer a discretionary luxury—it is a critical requirement for maintaining market relevance. Investing in flexible, software-driven robotic architectures today ensures that production infrastructure can quickly pivot to handle shifting consumer demands, unexpected raw material changes, and unpredictable global economic conditions tomorrow.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656