Global Cloud Applications Market Projected to Reach USD 1,596.16 Billion by 2030, Accelerating at a Compounding 19.3% CAGR

Industry Analysis and Comprehensive Market Forecast Signals Massive Multi-Sector Migration Toward Advanced SaaS and PaaS Architectures as Digital Transformation Becomes a Corporate Imperative.

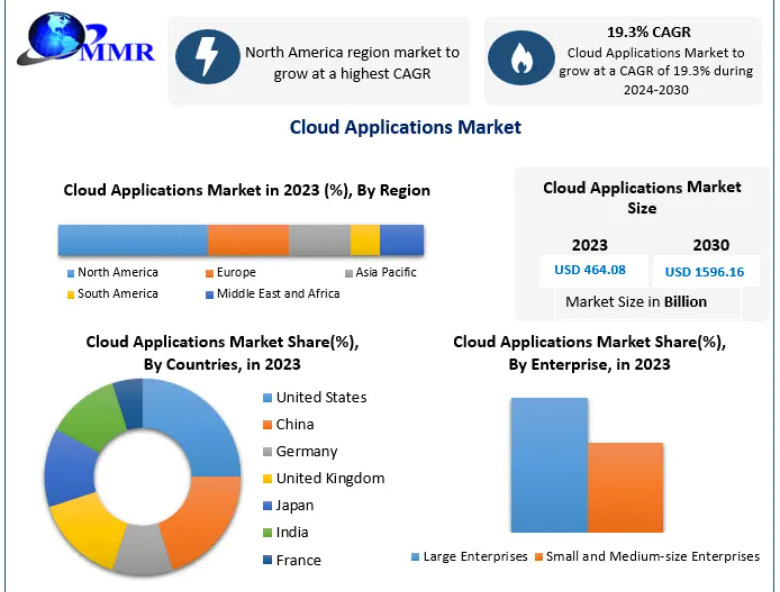

The global corporate ecosystem is undergoing a foundational paradigm shift as organizations discard legacy, on-premises systems in favor of flexible infrastructure. According to an extensive and highly detailed intelligence study published by Maximize Market Research, the Global Cloud Applications Market was valued at a commanding USD 464.08 Billion in 2023. This sector is positioned for monumental, uninterrupted growth over the forecast horizon, with overall revenue projected to climb at a compound annual growth rate (CAGR) of 19.3% from 2024 to 2030, culminating in an estimated global market valuation of USD 1,596.16 Billion by 2030.

This explosive trajectory highlights a critical commercial reality: cloud applications have evolved from a luxury option into a core element of modern corporate strategy. Today’s fast-moving business climate rewards organizations that can scale their computing resources instantaneously, lower capital expenditures (CapEx) in favor of predictable operational expenses (OpEx), and support highly distributed, global hybrid workforces. The definitive market analysis addresses the fundamental macro and microeconomic drivers, deep structural segment breakdowns, regional growth hubs, operational bottlenecks, and the shifting competitive landscape shaping this multi-billion-dollar market.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/116735/

Deciphering the Core Drivers: Why Enterprises are Migrating to Cloud Ecosystems

The ongoing shift toward cloud applications is driven by concrete business benefits that directly influence corporate balance sheets. At the front of these drivers are scalability, operational flexibility, remote accessibility, and workforce mobility.

Historically, business expansion required massive upfront investments in data centers, physical servers, and local network setups. If enterprise demand spiked unexpectedly, systems crashed; if demand dipped, expensive computing hardware sat idle. Cloud applications solve this structural mismatch through instant, elastic scaling. Organizations can adjust their active software capabilities, database capacities, and cloud computing environments in real time to match immediate transactional volumes. This level of adaptability provides middle-market enterprises and large conglomerates alike with the agility needed to survive modern market volatility.

Simultaneously, the rise of remote and hybrid work models has changed how corporate networks operate. Cloud applications provide universal access to mission-critical business data and enterprise applications from any geographic location with an internet connection. This has significantly enhanced cross-border collaboration, reduced project timelines, and improved operational efficiency.

Furthermore, modern cloud architectures act as the foundation for integrating next-generation technologies. Enterprises are leveraging cloud environments to deploy advanced Artificial Intelligence (AI), Machine Learning (ML) workflows, the Internet of Things (IoT), and big data analytics pipelines. This integration allows companies to access advanced automation capabilities without investing heavily in on-premises high-performance computing hardware. Combined with the automated failover configurations and disaster recovery protocols provided by top-tier cloud providers, it is clear why global enterprise software adoption continues to accelerate.

Segment Spotlight: Supply Chain Management (SCM) Leading the Digital Charge

An engine driving the growth of the cloud applications industry is the Supply Chain Management (SCM) segment. Based on the deep data mapping in the report, the cloud-based SCM segment captured a massive share of total market revenues in 2023.

The global supply chain shocks of recent years highlighted the vulnerabilities of old legacy systems. Modern multi-tier supply networks require immediate data transparency, predictive logistical insights, and synchronized communication between suppliers, factories, and distributors. Cloud-based SCM architectures provide businesses with real-time access to operational tracking metrics, enabling logisticians to make rapid decisions when shipping routes break down or demand changes unexpectedly.

Because top-tier cloud application developers build their software on standard data exchange protocols, cloud-hosted SCM applications easily remove old geographical and systemic silos. Teams can monitor inventory levels, manage supplier networks, track freight transit times, and process global procurement orders using any verified device worldwide. This real-time visibility turns supply chains into highly dynamic, responsive, and responsive operational assets that actively reduce overhead costs and optimize inventory management.

Sectoral Adoption: The Transformed Landscape of BFSI and Cloud Governance

From an end-user perspective, the Banking, Financial Services, and Insurance (BFSI) vertical held a dominant share of the global cloud applications market in 2023. Historically, the financial sector was slow to adopt public and hybrid cloud software due to strict data privacy mandates, strict regulatory frameworks, and worries over system vulnerability. However, the modern push for digital transformation has shifted financial services toward the cloud.

The massive growth of the BFSI segment is driven by a shift toward customer-centric financial experiences, digital retail banking, and decentralized wealth management solutions. Financial institutions use secure cloud ecosystems to manage vast amounts of customer data, process instant payment transactions, manage digital wallets, and run complex fraud-detection algorithms.

Cloud environments give financial networks the technical foundation to build open banking ecosystems and seamless consumer applications. By deploying cloud-based Customer Relationship Management (CRM) tools, automated underwriting software, and cloud-native accounting engines, financial institutions can shift away from maintaining legacy mainframes. Instead, they can focus their resources on creating innovative, secure, and regulatory-compliant digital banking experiences.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/116735/

Confronting the Restraints: Overcoming Security, Latency, and Integration Bottlenecks

Despite the market’s positive growth trajectory, enterprise decision-makers must navigate several ongoing market constraints, integration complexities, and operational challenges.

The primary hurdle for enterprise cloud migration is data security and compliance management. Transferring proprietary intellectual property, financial data, and personal identifiable information (PII) to shared public or hybrid cloud environments exposes companies to risks like data breaches, misconfigured access privileges, and complex compliance demands (such as GDPR, CCPA, and HIPAA). For risk-averse organizations, navigating data protection in a multi-tenant cloud environment remains a key concern that requires careful strategic planning.

Additionally, integrating legacy, on-premises applications with modern cloud deployments can be a complex technical task. Fragmented architectures often create data silos, slow down system communication, and lead to compatibility issues that require extensive custom engineering to fix.

Furthermore, cloud-dependent applications rely on stable internet connections. Network lag or unexpected downtime can impact application performance, disrupt user workflows, and threaten business continuity. To address these vulnerabilities, organizations are implementing modern cybersecurity tools, structured integration frameworks, redundant connectivity paths, and rigorous cost-optimization guidelines (FinOps) to capture the full economic value of their cloud assets.

Capitalizing on Future Frontiers: Advanced Analytics, AI Integration, and Hyper-Scalability

As the cloud application landscape matures, new growth opportunities are emerging around rapid code deployment, containerized microservices, and built-in predictive analytics.

Modern cloud platforms offer software developers pre-built frameworks, DevOps automation tools, and serverless computing structures. These tools allow development teams to build, test, and launch enterprise-grade software in a fraction of the time required by traditional development environments. This speed helps companies respond to shifting consumer behaviors, giving early adopters a distinct competitive advantage.

Additionally, cloud-native software vendors are embedding advanced data analytics and automated machine learning features directly into their enterprise software packages. Rather than requiring distinct data engineering teams to extract and analyze information, modern cloud business applications automatically turn unstructured corporate data into clear, actionable insights. This democratization of data enables executives to make proactive decisions, optimize operations, and design innovative products.

Furthermore, subscription-based Software-as-a-Service (SaaS) and Platform-as-a-Service (PaaS) business models provide developers with predictable, recurring revenue streams. This financial stability fuels ongoing research and development, ensuring a steady stream of product upgrades and feature additions for the enterprise buyers driving the market forward.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/global-cloud-applications-market/116735/

Regional Dominance: North America Captures the Market, Asia-Pacific Rises Rapidly

From a geographic standpoint, North America held the largest market share in 2023, establishing itself as the main hub for cloud application deployment. This dominance is due to several structural advantages, including early investments in advanced technologies, widespread high-speed internet infrastructure, and a large concentration of Fortune 500 corporations focused on digital business transformation.

Enterprises across the United States and Canada are rapid adopters of cutting-edge solutions like industrial IoT platforms, additive manufacturing setups, automated data processing tools, and AI-driven workflows. This regional focus, combined with the presence of major cloud hyperscalers (such as Microsoft, Amazon Web Services, and Google Cloud Platform), positions North America as a leading force in cloud application innovation and adoption throughout the 2024-2030 forecast period.

Concurrently, Europe—anchored by strong technology investments in the United Kingdom, Germany, France, and the Nordic countries—continues to show steady expansion. European organizations are actively prioritizing cloud adoption to improve operational flexibility, navigate strict regional data privacy rules, and drive digital-first corporate initiatives.

Meanwhile, the Asia-Pacific region is emerging as the fastest-growing market for cloud applications. Driven by rapid industrialization, expanding technology infrastructure, high mobile internet adoption, and pro-digital government policies across China, India, Japan, and Australia, demand for scalable cloud software is growing quickly. As regional enterprises expand their digital operations and upgrade legacy systems, the Asia-Pacific cloud software sector is positioned to outpace traditional regional growth rates over the coming decade.

Competitive Framework: How Tech Giants are Redefining the Enterprise Landscape

The global cloud applications market is highly competitive, led by prominent technology corporations driving innovation across the SaaS, PaaS, and IaaS layers. These market leaders compete on product features, customization options, system reliability, integration support, and pricing structures.

-

Microsoft Corporation: A dominant force in corporate cloud ecosystems, Microsoft provides a comprehensive suite of business applications and infrastructural tools via Microsoft Azure. Azure competes directly with top public cloud ecosystems while working alongside enterprise business software platforms like Microsoft Dynamics 365. This seamless integration makes it a popular choice for enterprises looking to connect administrative productivity tools with advanced cloud operations.

-

Oracle Corporation: Long recognized for its database technologies, Oracle has successfully transitioned into a major player in the cloud applications market. The Oracle Cloud portfolio offers fully integrated suites for Enterprise Resource Planning (ERP), Human Capital Management (HCM), and Customer Relationship Management (CRM). Oracle leverages its database strengths to deliver highly performant, secure, and scalable solutions tailored for large global enterprises.

-

Salesforce, Inc.: Holding a leading position in the global CRM space, Salesforce continues to shape the cloud market with highly customizable, scalable, customer-centric SaaS applications. Its focus on cloud-native customer software allows businesses of all sizes to manage sales processes, client services, and marketing data through a unified cloud workspace.

-

Google Cloud Platform (GCP): Operating as Alphabet's enterprise cloud division, GCP competes with Azure and AWS by focusing on advanced data analytics, artificial intelligence infrastructures, and containerized application deployments. Google’s deep expertise in machine learning makes its cloud tools attractive to data-driven enterprises seeking sophisticated predictive modeling capabilities.

Recent Breakthroughs and Pioneering Product Launches

To maintain market share and address changing enterprise needs, leading vendors are continuously launching advanced solutions and cross-industry software upgrades.

-

April 2022 — Salesforce CRM Analytics Launch: Salesforce introduced its advanced Customer Relationship Management (CRM) Analytics platform across its core industry verticals. This PaaS solution integrates predictive artificial intelligence directly into client workflows, enabling businesses to access real-time automated forecasting and customer insights without needing standalone data-science pipelines.

-

February 2022 — Oracle Supplier Rebate Management Release: Oracle officially unveiled its Supplier Rebate Management software module as an extension of the Oracle Fusion Cloud Channel Revenue Management ecosystem. This targeted cloud application automates complex commercial trade agreements, financial reconciliation steps, and supply procurement billing. The launch helps companies optimize supply chain investments while strengthening Oracle's position in the enterprise SaaS market.

Strategic Takeaways for Enterprise Decision-Makers

The insights in the Maximize Market Research report suggest that staying on legacy on-premises software introduces growing operational risks and long-term technical debt. For modern C-level executives, migrating to cloud applications is no longer an optional IT upgrade—it is a foundational business decision.

To maximize the return on cloud investments, executive leadership should adopt a structured, multi-phase cloud roadmap. Organizations should prioritize migrating high-impact, non-core applications first, allowing teams to build experience with cloud workflows before transitioning mission-critical legacy engines. Simultaneously, investing in modern APIs, establishing dedicated data governance teams, and using multi-cloud security frameworks will help safeguard data assets, prevent vendor lock-in, and ensure long-term business agility.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656