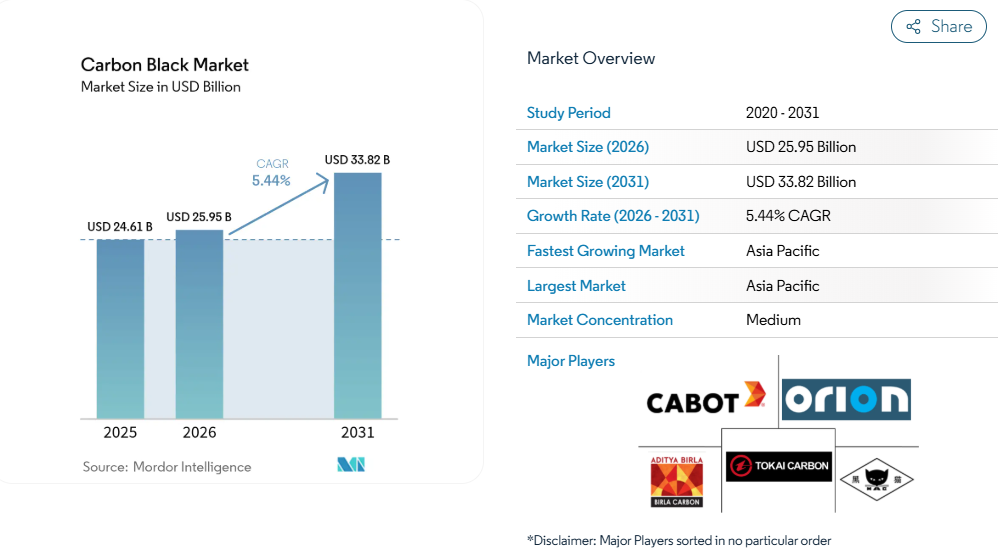

According to Mordor Intelligence, the carbon black market size is projected to increase from USD 25.95 billion in 2026 to USD 33.82 billion by 2031, reflecting steady demand across multiple end-use industries.

As manufacturers focus on improving product quality, reducing production costs, and meeting changing environmental expectations, suppliers are investing in efficient production processes and expanding regional manufacturing capacity. This carbon black market analysis highlights the factors supporting demand, the major application segments, competitive developments, and the companies shaping the industry. It also provides insights similar to those covered in a comprehensive carbon black industry report.

Key Trends Shaping the Carbon Black Market

Steady Demand from Tire Manufacturing

Tire production continues to be the foundation of the carbon black market. Carbon black improves tire strength, durability, wear resistance, and overall performance. As passenger vehicle production, commercial transportation, and replacement tire demand remain active across many regions, manufacturers continue to require reliable carbon black supplies.

Industrial rubber products such as belts, hoses, seals, and gaskets also contribute to consistent consumption, supporting stable demand across manufacturing industries.

Growing Use in Plastics and Specialty Applications

Carbon black is increasingly used in plastic products where color consistency, ultraviolet protection, and electrical conductivity are required. Manufacturers of packaging materials, automotive components, consumer products, and electrical equipment continue to incorporate specialty grades into their products.

The material is also finding wider use in coatings, inks, and battery-related applications, allowing suppliers to diversify beyond traditional rubber markets.

Regional Capacity Expansion Supports Supply

Manufacturers continue expanding production facilities closer to major customers, particularly across Asia-Pacific. Regional manufacturing investments improve supply reliability, reduce transportation challenges, and strengthen customer relationships.

This regional expansion allows producers to respond more efficiently to changing customer requirements while maintaining competitive supply chains.

Focus on Sustainable Manufacturing

Environmental expectations are encouraging producers to improve manufacturing efficiency and explore lower-emission production methods. Companies are also showing increasing interest in recovered carbon black and improved feedstock management to support sustainability goals.

Carbon Black Market Segmentation

The carbon black industry analysis covers several major segments based on production process and end-use application.

By process type, the market includes:

- Furnace Black

- Gas Black

- Lamp Black

- Thermal Black

Furnace black remains the most widely used production process because it supports large-scale manufacturing and serves a broad range of industrial applications. Other production methods continue to serve specialized customer requirements where unique product characteristics are needed.

By application, the market serves:

- Tires and industrial rubber products

- Plastics

- Toners and printing inks

- Coatings

- Textile fibers

- Other industrial applications

Tires and industrial rubber products continue to represent the largest share of demand due to carbon black's essential role in reinforcing rubber compounds. Plastics, coatings, and printing inks also remain important application areas where manufacturers value consistent pigmentation, durability, and protection against environmental exposure. Specialty applications continue expanding as customers seek improved material performance across a wider range of industries.

Unlock Localized Market Intelligence, Featuring Japan-Specific Report Editions

Geographically, Asia-Pacific remains the leading regional market, supported by large automotive manufacturing operations, expanding industrial production, and growing demand from plastics and rubber processing industries. Other regions continue to maintain stable demand through established manufacturing sectors and replacement markets.

Carbon Black Companies

The competitive landscape includes several established global manufacturers with extensive production capabilities and long-standing customer relationships. Companies continue focusing on production efficiency, regional expansion, specialty product development, and supply reliability.

- Cabot Corporation

- Birla Carbon

- Orion Engineered Carbons S.A.

- Tokai Carbon Co. Ltd

- Jiangxi Black Cat Carbon Black Co. Ltd

Many of these companies continue investing in manufacturing capacity, expanding specialty product portfolios, strengthening customer partnerships, and improving operational efficiency. Strategic investments in regional production facilities help them support customers more effectively while responding to changing demand patterns across automotive, plastics, coatings, and industrial markets. The competitive environment also reflects increasing attention toward sustainable production practices and specialty carbon black applications that offer higher value across multiple industries.

Conclusion

The carbon black market remains supported by steady demand from tire manufacturing while gradually expanding into plastics, coatings, battery materials, and other specialty applications. Manufacturers continue strengthening regional supply networks, improving production efficiency, and responding to customer demand for reliable and sustainable materials.

As automotive production, industrial manufacturing, and specialty material applications continue developing, the outlook remains positive for suppliers that balance operational efficiency with product quality and regional availability. Businesses seeking deeper market insights can benefit from a detailed carbon black industry report, while this carbon black market analysis highlights the major trends, competitive landscape, application segments, and industry direction that continue to shape global demand.