Before viewing a single property, before speaking to an estate agent, and often before even approaching a mortgage broker, there are two numbers every UK homebuyer should already know: what their monthly mortgage repayment will realistically look like, and how much stamp duty they'll owe on completion. A repayment mortgage calculator and a UK stamp duty calculator answer exactly these questions, and together they form the financial foundation that every other decision in the home-buying process should be built on.

Starting With What You Can Actually Afford Monthly

It's tempting to start house-hunting based on what a lender says you're approved to borrow, but the maximum loan amount a bank offers isn't necessarily the same as what feels comfortable month to month. A repayment mortgage calculator bridges that gap by turning loan amount, interest rate, and term into a clear monthly figure that can be tested against real household finances rather than an abstract borrowing limit.

The calculation depends on a few core factors:

- How much you're borrowing the property price minus your deposit

- The interest rate on offer fixed-rate deals lock in a rate for an initial period, while variable and tracker rates can move with the market

- How long you're borrowing for commonly 25 years, though terms from 15 to 35+ years are available depending on age and lender criteria

- Whether it's repayment or interest-only repayment mortgages steadily pay down the loan itself, while interest-only mortgages (typically used by landlords) leave the full balance owed at the end unless a separate repayment vehicle is in place

What makes a calculator genuinely useful isn't just producing one number it's the ability to test multiple scenarios quickly. Increasing the deposit by even a few thousand pounds, or comparing a 25-year term against a 30-year term, often reveals meaningful differences in monthly affordability that aren't obvious just from looking at headline mortgage rates advertised by lenders.

The Cost Buyers Forget Until It's Too Late

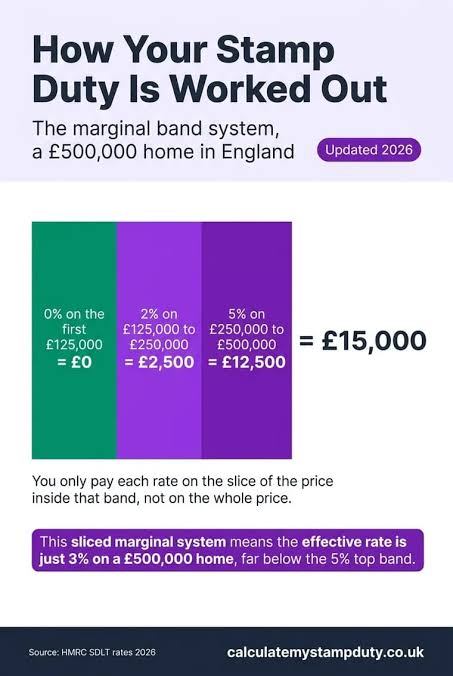

Stamp Duty Land Tax is one of the most commonly overlooked costs in the entire home-buying process, largely because it doesn't show up anywhere in the ongoing monthly budget conversation it's a single lump sum due shortly after completion, and for many buyers it comes as an unwelcome surprise right when the rest of their cash has already gone toward the deposit and moving costs.

A UK stamp duty calculator removes that uncertainty by applying the current tiered tax bands directly to a property's purchase price. A few details significantly affect the final figure:

- Tiered rate bands different portions of the purchase price are taxed at increasing rates, rather than one flat percentage applied to the whole amount

- First-time buyer relief many buyers purchasing their first property qualify for reduced rates or full exemption up to a certain price threshold, which can substantially lower or even eliminate the amount owed

- Additional property surcharge anyone purchasing a second home, holiday home, or buy-to-let investment typically pays an extra percentage on top of the standard rate

- Devolved nation differences Scotland and Wales apply their own separate property transaction taxes, with their own thresholds that differ from the rates used in England and Northern Ireland

Because these thresholds and rates are subject to periodic government changes, checking an up-to-date calculator at the time of purchase rather than relying on figures from a previous purchase or a rough online estimate is the only reliable way to know the actual amount owed.

Why Checking Both Early Changes the Whole Process

Buyers who only calculate their monthly mortgage affordability often build a budget that looks solid on paper, only to discover the stamp duty bill eats significantly into funds they'd earmarked for moving costs, furniture, or renovations. Checking both figures together, early in the process, changes the entire approach to house-hunting:

- It sets a genuinely realistic overall budget, not just a monthly affordability ceiling

- It allows for accurate comparison between properties at different price points, since stamp duty increases disproportionately as price crosses each tax band threshold

- It prevents last-minute scrambling for funds close to completion, when there's little flexibility left to adjust

- It gives buyers stronger negotiating confidence, since they understand the true all-in cost of any offer they make

Final Thoughts

The excitement of house-hunting often overshadows the financial groundwork that should come first, but the buyers who navigate the process most smoothly are almost always the ones who ran the numbers before they started looking. A repayment mortgage calculator shows exactly what a property will cost every month for years to come, while a UK stamp duty calculator reveals the one-off tax bill due almost immediately after completion. Checking both before making an offer isn't just good practice it's what separates a well-planned purchase from a financially stressful one.