The Global Occlusion Devices Market has emerged as a crucial segment within the medical devices industry, driven by the rising prevalence of cardiovascular and neurovascular disorders. Occlusion devices are specialized medical implants designed to block or close abnormal blood flow within the heart or blood vessels. These devices play a pivotal role in minimally invasive surgeries, reducing the risk of complications and improving patient outcomes. With advancements in medical technology and increasing awareness about early intervention procedures, the market for occlusion devices has seen significant growth over the past decade.

In 2024, the global market is projected to reach USD 4.0 billion and is expected to expand to an estimated USD 6.5 billion by 2033, reflecting a compound annual growth rate (CAGR) of 5.5%. This growth trajectory highlights the rising demand for efficient treatment solutions for cardiovascular anomalies, neurovascular defects, and other chronic conditions that necessitate the use of occlusion devices.

The market expansion is primarily fueled by advancements in minimally invasive procedures, a growing geriatric population, and a significant increase in the incidence of congenital heart diseases. Additionally, hospitals and specialized cardiac centers are increasingly adopting cutting-edge technologies to improve surgical precision, reduce patient recovery times, and optimize clinical outcomes.

Key Drivers Shaping the Occlusion Devices Market

Several factors are driving the growth of the global occlusion devices market. Understanding these drivers provides insights into the potential opportunities for stakeholders and healthcare providers in this evolving space.

Rising Prevalence of Cardiovascular and Neurovascular Disorders

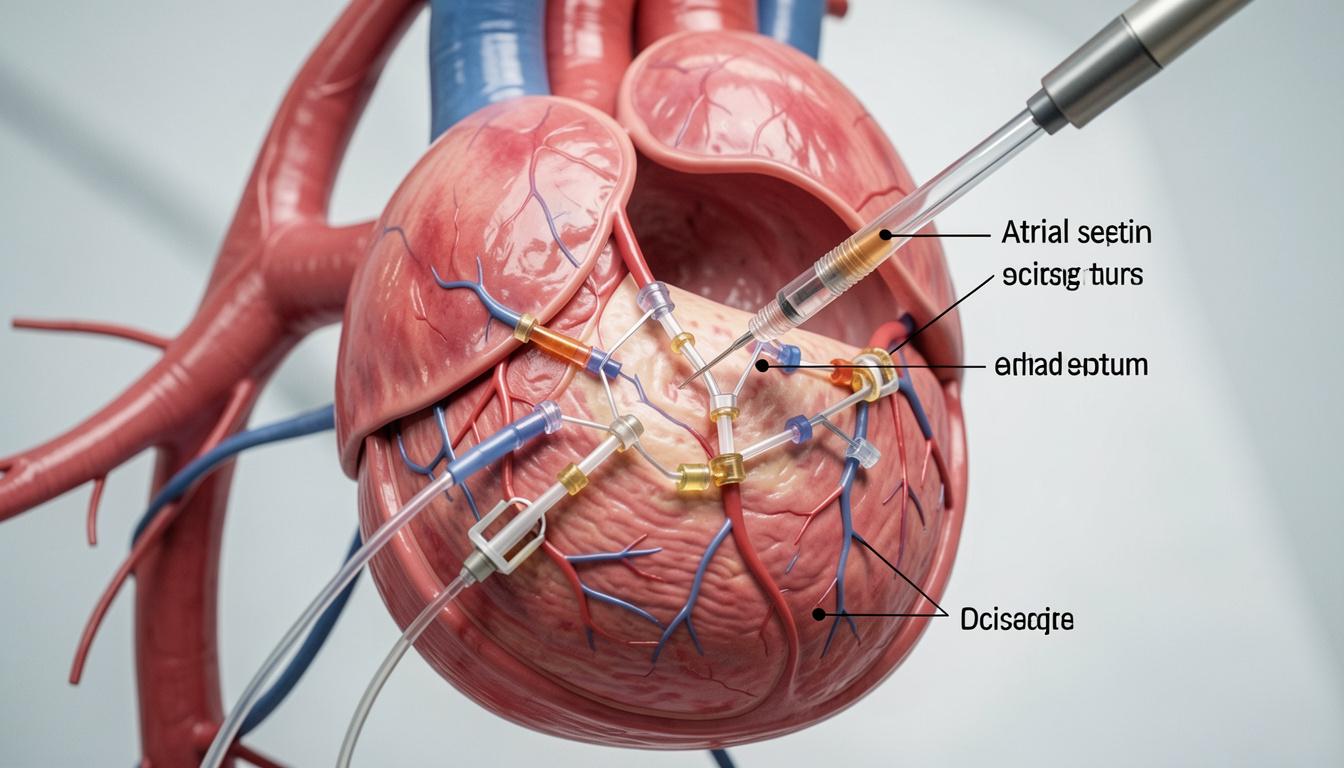

Cardiovascular diseases, including heart failure, atrial septal defects (ASDs), and patent foramen ovale (PFO), are among the leading causes of morbidity worldwide. Neurovascular conditions such as cerebral aneurysms also necessitate the use of occlusion devices to prevent complications. As the incidence of these conditions rises, healthcare providers increasingly rely on minimally invasive devices to manage patients effectively. Occlusion devices offer a safe, less invasive alternative to open-heart surgeries, reducing hospitalization times and post-operative complications.

Advancements in Minimally Invasive Procedures

The shift toward minimally invasive cardiac and vascular procedures is a significant driver of market growth. Occlusion devices, often deployed through catheter-based techniques, enable surgeons to close abnormal blood vessels without extensive surgery. These advancements not only improve patient safety but also reduce recovery periods, hospital stays, and overall treatment costs. Technological innovations, including bioresorbable materials and enhanced device design, further enhance the efficacy and safety of occlusion devices.

Government Reimbursements and Supportive Policies

Reimbursement policies play a crucial role in promoting the adoption of occlusion devices. In developed markets like North America and Europe, favorable insurance schemes and government support reduce the financial burden on patients, encouraging the use of advanced therapeutic devices. These policies have accelerated the penetration of occlusion devices in hospitals and specialized cardiac centers, supporting overall market growth.

Technological Advancements and Product Innovation

The continuous evolution of occlusion devices has expanded their applications across multiple therapeutic areas. Innovations such as shape-memory alloys, coated implants to prevent thrombosis, and improved catheter delivery systems are driving higher adoption rates. Manufacturers are also focusing on developing devices that are easier to deploy and customizable according to patient anatomy, thereby increasing the efficiency and success of surgical procedures.

Market Segmentation

The global occlusion devices market can be segmented based on device type, application, end-user, and geography. Each segment offers unique opportunities for market players to cater to the specific needs of patients and healthcare providers.

By Device Type

-

Septal Occluders – Used primarily for closing atrial or ventricular septal defects, these devices are widely adopted due to their proven efficacy in pediatric and adult patients.

-

Vascular Plugs – Utilized in neurovascular and peripheral vascular applications, vascular plugs are gaining traction for their ability to treat aneurysms and vessel malformations effectively.

-

Patent Foramen Ovale (PFO) Occluders – Specifically designed for the closure of PFOs, these devices are increasingly used to prevent strokes in patients with cryptogenic conditions.

-

Others – This includes novel occlusion devices designed for emerging applications, incorporating bioresorbable materials and advanced coatings.

By Application

-

Cardiovascular Diseases – The most significant application segment, driven by the rising prevalence of congenital and acquired heart defects.

-

Neurovascular Disorders – Increasing awareness of cerebral aneurysms and related conditions is boosting demand for neurovascular occlusion devices.

-

Peripheral Vascular Disorders – Growing adoption in peripheral interventions, such as arteriovenous malformations and vascular embolizations.

By End-User

-

Hospitals – The largest end-user segment, owing to the availability of specialized cardiac and neurovascular surgery centers.

-

Cardiac Centers – High adoption due to the focus on minimally invasive procedures and advanced patient care.

-

Ambulatory Surgical Centers – Growing preference for outpatient procedures contributes to the increasing use of occlusion devices.

Download a Complimentary PDF Sample Report: https://dimensionmarketresearch.com/request-sample/occlusion-devices-market/

Regional Analysis

North America

North America is expected to dominate the occlusion devices market in terms of revenue over the forecast period. The region accounted for a 34.5% revenue share in 2024, driven by supportive reimbursement policies that encourage minimally invasive interventions, particularly in the United States and Canada. A rising prevalence of cardiovascular and neurovascular diseases, coupled with the presence of advanced healthcare infrastructure, ensures high adoption rates for these devices. Additionally, continuous technological innovations and significant investments in R&D by key players further strengthen North America’s market position.

Europe

Europe is witnessing steady growth in the occlusion devices market, propelled by the rising geriatric population and the growing incidence of heart-related disorders. Countries such as Germany, France, and the UK have well-established healthcare systems and reimbursement frameworks that facilitate the adoption of advanced medical devices. Additionally, growing awareness about early intervention in congenital heart defects contributes to market expansion.

Asia-Pacific

The Asia-Pacific region is expected to demonstrate significant growth, driven by rising healthcare expenditure, increasing patient awareness, and improving medical infrastructure in countries such as China, India, and Japan. The adoption of minimally invasive procedures is gaining momentum, and several government initiatives to enhance cardiac care access further fuel the demand for occlusion devices.

Latin America

Latin America is emerging as a potential growth market due to increasing awareness of cardiovascular diseases and gradual improvements in healthcare facilities. Although market penetration is relatively low compared to North America and Europe, rising investments in healthcare infrastructure and the availability of cost-effective devices are expected to drive growth.

Middle East & Africa

The Middle East and Africa present moderate growth opportunities. Although adoption is slower due to economic constraints and limited healthcare infrastructure, rising incidences of cardiovascular disorders, coupled with improving medical facilities and government initiatives, provide avenues for market development.

Competitive Landscape

The global occlusion devices market is highly competitive, with several key players focusing on product innovation, strategic partnerships, and acquisitions to strengthen their market position. Companies are investing in R&D to develop advanced devices that offer improved patient outcomes, reduced procedure times, and lower complication rates. The competitive landscape is also shaped by mergers and acquisitions, collaborations with hospitals and research institutions, and expansion into emerging markets.

Market Challenges

Despite promising growth, the occlusion devices market faces several challenges:

-

High Device Cost – Advanced occlusion devices are expensive, which can limit adoption, particularly in developing countries.

-

Regulatory Hurdles – Stringent regulatory approvals and compliance requirements can delay product launches.

-

Limited Awareness – In some regions, lack of awareness among healthcare professionals and patients regarding the benefits of minimally invasive occlusion devices hinders adoption.

-

Risk of Complications – Although minimally invasive, improper device deployment or patient-specific anatomical challenges may lead to procedural complications.

Future Outlook

The global occlusion devices market is poised for sustained growth over the next decade. Increasing prevalence of cardiovascular and neurovascular disorders, coupled with technological advancements and favorable reimbursement policies, will continue to drive demand. Additionally, expanding applications in pediatric cardiology and peripheral vascular interventions present untapped opportunities. With manufacturers focusing on innovation, patient-specific customization, and minimally invasive solutions, the market is expected to witness exponential growth in both developed and emerging regions.

Frequently Asked Questions (FAQs)

1. What are occlusion devices used for?

Occlusion devices are used to block or close abnormal blood flow in the heart or blood vessels. They are commonly applied in treating conditions like atrial septal defects, patent foramen ovale, and aneurysms.

2. Which regions dominate the occlusion devices market?

North America currently dominates the market due to favorable reimbursement policies, advanced healthcare infrastructure, and a high prevalence of cardiovascular and neurovascular disorders.

3. What are the key trends in occlusion devices?

Key trends include minimally invasive procedures, use of bioresorbable materials, advanced catheter delivery systems, and patient-specific device customization.

4. What factors are driving market growth?

Market growth is driven by rising cardiovascular disease prevalence, technological advancements, increasing awareness, and supportive government policies.

5. What challenges do occlusion device manufacturers face?

Manufacturers face high device costs, regulatory hurdles, limited awareness in some regions, and potential procedural complications.

Key Insights and Conclusion

The Global Occlusion Devices Market is on a strong growth trajectory, projected to reach USD 6.5 billion by 2033. With the increasing prevalence of cardiovascular and neurovascular disorders, a shift toward minimally invasive procedures, and advancements in device technology, the market presents significant opportunities for manufacturers, healthcare providers, and investors. North America leads the market, but Asia-Pacific and other emerging regions are expected to contribute substantially to future growth.

As healthcare systems worldwide continue to prioritize patient safety, efficiency, and better clinical outcomes, occlusion devices will remain a vital solution in managing complex cardiovascular and neurovascular conditions. Manufacturers focusing on innovation, affordability, and accessibility are likely to achieve a competitive edge in this expanding market.

Purchase the report for comprehensive details: https://dimensionmarketresearch.com/checkout/occlusion-devices-market/