Global Torque Vectoring Market Extends Beyond USD 10 Billion Base: Next-Generation Drivetrain Control Systems Revolutionize Automotive Dynamics and EV Architectures

Executive Summary: The Dawn of Intelligent Drivetrain Dynamics

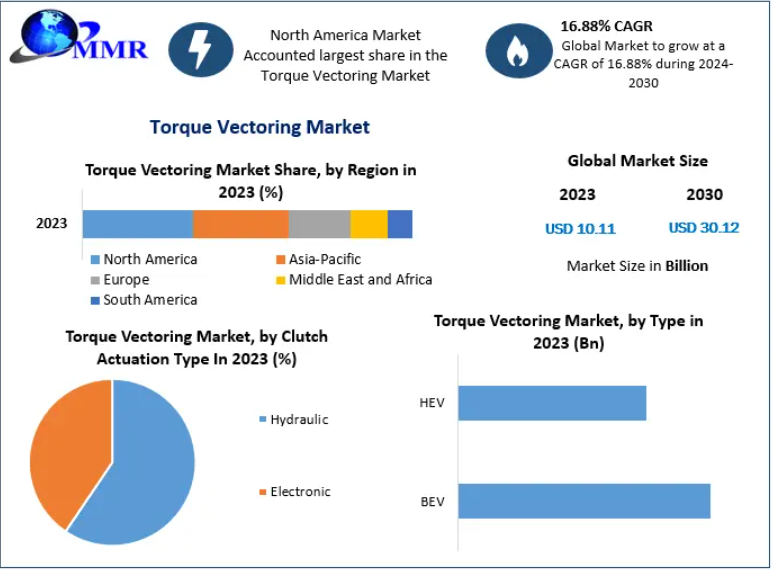

The evolution of modern vehicle control systems has transcended basic mechanical stabilization, establishing software-defined and electronically controlled power distribution as the new baseline for automotive innovation. According to an extensive market analysis published by Maximize Market Research, the global Torque Vectoring Market is undergoing a profound structural shift. Valued at an impressive baseline of USD 10.11 Billion, the market is poised to experience an aggressive compound annual growth rate (CAGR) of 16.88% through the forecast horizon.

This highly targeted press release delivers an exhaustive, SEO-optimized breakdown of the market forces, segmentation parameters, competitive landscape, and regulatory paradigms shaping the torque vectoring industry. Designed specifically for chief technology officers (CTOs), tier-1 automotive suppliers, institutional investors, and digital marketing professionals looking to optimize their industry insights, this analysis establishes a definitive blueprint for strategic corporate decision-making.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/185108/

Defining Torque Vectoring: A Technological Imperative

At its core, torque vectoring is an advanced drivetrain technology that dynamically varies the torque applied to each driven wheel. Unlike conventional open differentials or electronic stability control (ESC) systems—which rely heavily on braking individual wheels to correct skidding (a passive, energy-depleting process)—torque vectoring actively transfers power to where it can be utilized most effectively.

During cornering maneuvers, an active torque vectoring system channels additional rotational force to the outside wheel while reducing torque to the inside wheel. This creates a controlled yaw moment, significantly reducing understeer, sharpening steering response, and drastically improving vehicle lateral acceleration without shedding linear velocity.

Core Market Drivers: Fueling High-Velocity Growth

The sustained expansion of the torque vectoring sector is not a localized or transient phenomenon. It is propelled by a convergence of technological breakthroughs, shift in consumer preferences, and rigorous global safety frameworks.

1. The Proliferation of Multi-Motor Electric Vehicle (EV) Architectures

The global automotive matrix is transitioning rapidly toward electrification. Traditional internal combustion engine (ICE) drivetrains require complex mechanical assemblies—such as multi-plate wet clutches, hydraulic pumps, and heavy differentials—to execute torque vectoring.

Conversely, modern Electric Vehicles utilizing dual-motor, triple-motor, or quad-motor configurations can achieve electronic torque vectoring purely via software. By independently modulating the current fed to distinct wheel-hub or axle-mounted motors, an EV can adjust torque distribution in microseconds. This near-instantaneous response time makes electrification the primary structural catalyst for the torque vectoring ecosystem.

2. Escalating Regulatory Pressure on Passive and Active Safety Standards

Global safety watchdogs, including Euro NCAP, NHTSA, and CNCAP, continue to introduce increasingly stringent testing parameters for vehicle rollover immunity, collision avoidance, and wet-weather handling. Because torque vectoring continuously optimizes tire tractive capability, it acts as an invisible safety layer. By preventing the loss of traction before electronic stability systems are required to intervene, torque vectoring lowers accident probabilities, allowing original equipment manufacturers (OEMs) to secure highly coveted five-star safety ratings.

3. Consumer Demand for Premium Crossovers and High-Performance SUVs

The global automotive consumer profile has skewed dramatically toward Sports Utility Vehicles (SUVs) and Crossover Utility Vehicles (CUVs). Due to their elevated ride height and higher center of gravity, these vehicles are naturally prone to body roll and sluggish transient handling. To match the nimble driving characteristics of traditional sports sedans, premium OEMs are integrating advanced active torque vectoring differentials. This ensures that large-format utility vehicles handle predictably, safely, and dynamically across both urban corridors and rugged terrains.

Comprehensive Market Segmentation Matrix

To provide clarity and actionable data for institutional forecasting, the global torque vectoring ecosystem is segmented across three primary vectors: Technology Type, Propulsion System, and Vehicle Architecture.

By Technology Type: Active vs. Passive Systems

-

Active Torque Vectoring Systems (ATVS): Dominating the global market share, active systems employ electronically controlled clutches, planetary gearsets, or individual electric motors to manually send a disproportionate amount of torque to a specific wheel. This segment commands the highest revenue share due to its capability to operate under both acceleration and deceleration phases, providing unparalleled driving dynamics.

-

Passive Torque Vectoring Systems (PTVS): Often referred to as brake-actuated torque vectoring, this approach leverages the vehicle's existing anti-lock braking system (ABS) infrastructure to pinch the brakes on the inside wheel during a turn. While highly cost-effective and lighter than mechanical active systems, it inherently wastes kinetic energy as thermal energy, positioning it as an entry-level solution for budget-conscious vehicle segments.

By Propulsion System: Electrification Takes the Wheel

-

Battery Electric Vehicles (BEVs) and Hybrid Electric Vehicles (HEVs): This is the fastest-growing sub-segment within the propulsion category. The native compatibility of electric drivetrains with digital torque management removes mechanical friction points and lowers manufacturing assembly complexities over the long term.

-

Internal Combustion Engine (ICE): While losing relative market share to electric powertrains, the absolute volume of ICE vehicles equipped with mechanical electronic limited-slip differentials (eLSD) remains substantial, particularly within the heavy commercial truck and premium luxury performance categories.

By Vehicle Architecture: Volume vs. Margin

-

Passenger Cars: Comprising high-performance hatchbacks, executive sedans, and grand tourers. Volume growth is driven by consumer appetite for enthusiast-level driving dynamics.

-

Light Commercial Vehicles (LCVs) & Premium SUVs: This segment represents a significant revenue engine. The integration of advanced all-wheel-drive (AWD) systems with dedicated torque-selective differentials provides essential security for heavy vehicles navigating adverse weather or off-road conditions.

-

Regional Landscape Analysis: Geopolitical Trends and Hotspots

The application and adoption rates of torque vectoring technologies vary considerably by geographic region, driven by localized supply chain variations and consumer buying patterns.

Asia-Pacific: The Volume Epicenter

The Asia-Pacific region stands as the largest revenue generator and manufacturing hub for the global automotive sector. Driven by the explosive growth of high-technology electric vehicle brands in China, alongside established automotive manufacturing footprints in Japan and South Korea, APAC commands a leading stake in torque vectoring adoption. The rapid build-out of localized supply chains for tier-1 differential components has brought down the overall bill-of-materials (BOM) cost, allowing torque vectoring to migrate from luxury vehicles down to mid-tier consumer segments.

North America: Driven by Utility and Performance

In the United States and Canada, the market is characterized by a high penetration rate of full-size pickup trucks and large, premium SUVs. Consumers in these regions prioritize high towing capacities, foul-weather reliability, and sophisticated off-road capabilities. Consequently, the demand for electronic axles (e-Axles) capable of executing robust torque vectoring across demanding landscapes remains exceptionally high.

Europe: Engineering-Led Premium Integration

Europe represents the spiritual home of advanced chassis engineering and luxury performance vehicle validation. Major automotive conglomerates based out of Germany, Italy, and the United Kingdom utilize advanced torque vectoring setups as a core brand differentiator. European development cycles focus on high-speed stability, variable track-handling profiles, and integrating torque vectoring networks into complex multi-domain central control units.

-

Competitive Intelligence: Key Market Players

The global torque vectoring competitive grid is characterized by heavy consolidation among institutional Tier-1 automotive suppliers who possess deep intellectual property assets in driveline engineering. Key industry leaders driving innovation include:

-

GKN Automotive: A pioneer in sophisticated all-wheel-drive configurations and e-Drive systems, consistently leading the market with its Twinster technology.

-

BorgWarner Inc.: Known for its advanced electronic limited-slip differentials (eLSD) and cross-axle torque management systems optimized for both ICE and hybrid platforms.

-

ZF Friedrichshafen AG: A dominant force in intelligent chassis and driveline components, delivering highly integrated axle systems for premium European electric vehicles.

-

Magna International Inc.: Renowned for its modular powertrain systems, enabling OEMs to seamlessly implement torque-vectoring architectures across disparate vehicle segments.

-

Continental AG & Robert Bosch GmbH: Utilizing their deep expertise in electronic control units (ECUs), vehicle dynamics software, and brake-actuated stability management systems to dominate the passive and software-defined torque vectoring domains.

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/torque-vectoring-market/185108/

Technical Hurdles and Market Constraints

Despite the clear benefits to handling, safety, and performance, widespread adoption across entry-level commercial vehicles faces several structural headwinds:

1. Cost Constraints and Complexity

Developing and calibrating an active mechanical torque vectoring system requires significant upfront research and development capital. The addition of specialized clutch packs, electronic actuators, and dedicated cooling circuits increases the manufacturing cost per vehicle unit, making it difficult to justify on low-margin economy cars.

2. Weight and Packaging Issues

Mechanical torque-vectoring differentials are inherently heavier than standard open differentials. In an industry where engineering teams fight for every gram of weight reduction to optimize fuel economy and maximize EV battery range, the added mass of mechanical systems must be carefully balanced against its dynamic advantages.

3. Thermal Management Profiles

Continuous, high-frequency torque modulation across high-performance clutch packs generates immense friction and thermal energy. Developing robust, localized cooling systems that prevent thermal degradation during extended track sessions or harsh off-road excursions requires sophisticated fluid dynamics engineering and expensive synthetic lubricants.

Future Outlook: The Next Phase of Vectoring Technology

The horizon of torque vectoring is directly tied to the development of Software-Defined Vehicles (SDVs). Looking ahead, the industry is moving away from standalone localized differential controllers toward centralized, AI-driven vehicle domain computers.

By feeding real-time telemetry—such as steering wheel angle, lateral G-forces, individual wheel-speed sensors, and forward-looking camera radar data—into a unified neural chassis control loop, future torque vectoring systems will proactively adapt to road conditions before the vehicle enters a corner. Predictive torque allocation will enhance passenger comfort, increase regenerative braking efficiency by up to 15%, and unlock new handling horizons for autonomous driving pods operating in unpredictable weather conditions.

Strategic Recommendations for Automotive Executives

To capitalize on the accelerating torque vectoring market, stakeholders should adopt a multi-pronged strategic approach:

-

Prioritize Modular e-Axle Solutions: Tier-1 suppliers must design modular, drop-in e-Axle systems that bundle the electric motor, power inverter, transmission, and active torque vectoring unit into a single, compact package to lower OEM assembly friction.

-

Invest Heavily in Calibration Software: As mechanical configurations give way to multi-motor software control, competitive advantage will shift from physical gear manufacturing to precision calibration software algorithms.

-

Form Strategic Consortia with EV Specialists: Traditional driveline component manufacturers should establish joint ventures with software developers and battery management system providers to optimize the inter-connectivity of powertrain efficiency and vehicle dynamics.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

-

-

COntact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656