Global Connected Car Devices Market Poised to Hit USD 219.02 Billion by 2030, Fueled by an Unprecedented 16.1% CAGR

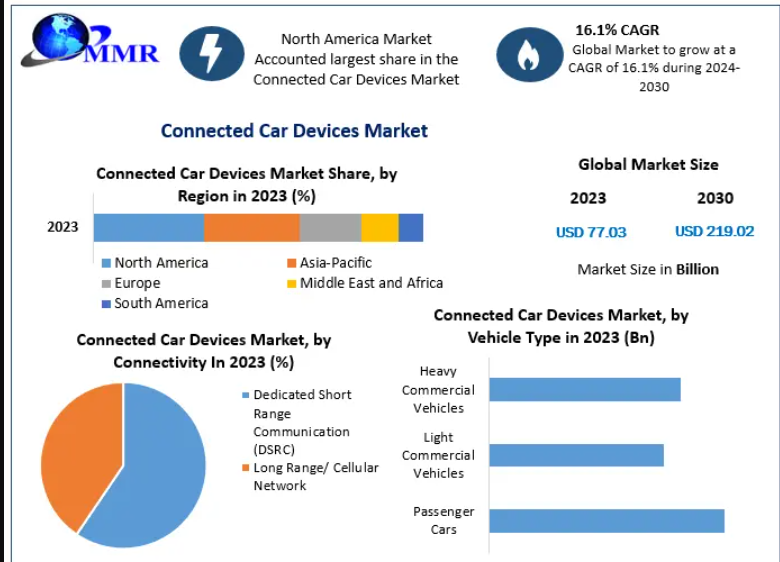

In an era defined by rapid digital transformation and the widespread expansion of the Internet of Things (IoT), the global automotive landscape is undergoing a paradigm shift. According to an extensive and highly detailed intelligence report published by Maximize Market Research, the Global Connected Car Devices Market was valued at USD 77.03 Billion in 2023 and is projected to reach an impressive USD 219.02 Billion by 2030, exhibiting a robust Compound Annual Growth Rate (CAGR) of 16.1% over the forecast matrix (2024–2030).

This comprehensive market analysis highlights a crucial shift from traditional mechanical vehicle platforms to data-driven mobility ecosystems. Modern vehicles are transitioning into highly sophisticated, rolling internet-connected nodes. The convergence of high-speed telecommunications, predictive machine learning models, and strictly enforced government safety regulations is fundamentally altering how consumers interact with their vehicles, establishing connected hardware as a core element of modern automotive engineering.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/1287/

Market Overview and Paradigm Shifts in Connected Mobility

The modern automobile has evolved far beyond its core function of mechanical transportation. Today, vehicles serve as intelligent, highly interactive communication hubs. Driven by advanced electronic control units (ECUs), integrated eSIM modules, and high-fidelity sensor arrays, the connected vehicle environment continuously captures, processes, and transmits critical operational data. These built-in ecosystems allow vehicles to monitor driver alertness through facial recognition and body posture tracking, execute immediate over-the-air (OTA) software updates, and deliver proactive anti-theft tracking notifications straight to a user's mobile device.

This technological progress is fundamentally changing consumer expectations and the priorities of original equipment manufacturers (OEMs). Features that were once considered premium upgrades—such as intelligent route navigation, remote vehicle diagnostics, and real-time cabin environmental adjustments—are quickly becoming standard baseline expectations across global vehicle lines. As high-speed 5G networks roll out worldwide, the communication flow between vehicles and cloud infrastructure is scaling rapidly, laying the essential technical foundation for fully autonomous driving environments.

Core Market Dynamics: Identifying Key Growth Drivers and Catalysts

1. Widespread Integration of Telecom Services and High-Speed Cellular Architecture

The rapid integration of telecommunications infrastructure into automotive manufacturing serves as a major catalyst for market expansion. Leading global automakers, such as BMW and Tesla, continue to integrate dedicated SIM cards and embedded telematics directly onto production lines. This allows cars to access network services independently without needing a tethered mobile phone. This architecture opens up significant commercial opportunities for global telecom providers, who are expanding beyond consumer mobile plans to supply high-bandwidth, low-latency data pipelines explicitly designed for enterprise automotive systems.

2. Rising Security Mandates, Theft Mitigation, and Public Safety Standards

Rising numbers of traffic incidents and vehicle thefts have turned advanced automotive safety technology from a premium option into a crucial regulatory requirement. Integrated diagnostic tools can spot internal component friction, battery degradation, and sudden system issues before they lead to structural failures or accidents on the road. Furthermore, if a vehicle break-in or unauthorized movement occurs, automated sensors send instant alerts to owner dashboards and emergency services, a capability that is significantly lowering insurance risks and driving up consumer demand.

3. Rapid Growth in Emerging Geographies and EV Ecosystems

Emerging markets, particularly across India and China, are experiencing significant infrastructure shifts driven by a rising middle class, an expanding young demographic, and an increasing focus on electric vehicles (EVs). India is quickly emerging as a major hub for shared mobility platforms, setting up a strong foundation for autonomous and electrified vehicle fleets. At the same time, regional export data confirms a steady, long-term growth trend in automotive manufacturing, highlighting a substantial market opportunity for aftermarket telematics and integrated electronic components.

Technical Segment Analysis: Technology, Connectivity, and Vehicle Types

Driver Assistance Systems (ADAS) Capture Dominant Market Share

From a technological perspective, the Driver Assistance Systems (ADAS) segment held the largest portion of the global market share in 2023 and is projected to maintain its market lead through 2030. This sector encompasses critical safety features, including lane departure warning systems, blind-spot detection, automated parking assistance, road sign recognition, and pedestrian safety sensors. Within this category, Adaptive Cruise Control (ACC) connectivity solutions are growing at the fastest rate, driven by a combination of falling hardware costs and cloud-based analytical software.

Regulatory Directives Driving Embedded Connectivity Solutions

Crucial applications like automated emergency calls (eCall) and deep-dive remote vehicle diagnostics cannot function effectively without reliable, factory-installed embedded communication systems. As a result, regulatory actions around the world are driving rapid adoption of this technology. For example, the European Union's mandate making eCall systems mandatory on all new passenger vehicle models has accelerated production timelines. Similar telematics requirements emerging across Brazil, Russia, and China are shifting the market toward standardized, factory-installed connected hardware.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐏𝐃𝐅 𝐁𝐫𝐨𝐜𝐡𝐮𝐫𝐞 @https://www.maximizemarketresearch.com/request-sample/1287/

Regional Performance Metrics and Geo-Economic Insights

North America: Leading the Way in Software Innovation and Infrastructure Adoption

North America continues to be a major revenue-generating hub for connected car technologies, driven by high consumer tech adoption and advanced transport networks. In the United States, deep market penetration of ADAS features, combined with extensive testing of autonomous commercial vehicle fleets, keeps the region at the forefront of the industry. Additionally, as initial factory subscriptions expire, a growing secondary market for connected vehicle software renewals is emerging, creating sustainable, long-term recurring revenue models for providers across the continent.

Asia-Pacific: The World's Fastest-Growing Mobility Engine

The Asia-Pacific region is experiencing the fastest revenue growth worldwide, with China and India serving as the primary manufacturing and consumption hubs. China's leading position in global production is supported by strong domestic electronics supply chains and state-supported smart city infrastructure projects. Meanwhile, India's changing transportation landscape—marked by a major shift toward vehicle electrification and cleaner energy alternatives—presents an ideal environment for large-scale deployments of connected fleet management tools.

Strategic Recommendations for Corporate Leaders and Investors

To capitalize on this 16.1% CAGR growth path, corporate decision-makers and technology investors should consider focusing on three key strategic priorities:

-

Prioritize Edge-Computing and Low-Latency Data Architecture: Engineering teams should focus on building hardware that processes critical safety data right on the vehicle edge. This ensures immediate split-second reactions for collision avoidance, while reserving broader cloud pipelines for non-urgent tasks like infotainment updates and long-term maintenance tracking.

-

Develop Scalable Aftermarket Telematics Portfolios: With millions of older vehicles still active on global roads, there is a massive commercial opportunity for secure, plug-and-play aftermarket telematics devices. These components allow older fleets to access modern fleet management and safety metrics without requiring a complete vehicle replacement.

-

Establish Proactive Security Frameworks: As vehicles become more reliant on software, they face increased vulnerability to cyber threats. Implementing robust end-to-end encryption across vehicle-to-everything (V2X) communication lines is essential for protecting passenger safety and maintaining long-term brand trust.

Detailed Competitive Landscape and Key Market Leaders

The global connected car devices marketplace features a highly competitive mix of established tier-1 automotive component suppliers, specialized semiconductor firms, and innovative software developers. Key industry players are actively pursuing strategic mergers, acquisitions, and joint ventures to broaden their technological capabilities, with a particular focus on expanding over-the-air (OTA) software systems and unified cloud diagnostics.

Connected Car Devices Market, Key Players are

1. Continental AG

2. Denso Corporation

3. Delphi Automotive, PLC

4. Robert Bosch GmbH

5. Autoliv Inc.

6. Valeo SA

7. Tesla

8. Volkswagen

9. Porsche

10. General Motors

11. Autoliv, Inc.

12. Continental AG

13. Delphi Automotive PLC

14. Denso Corporation

15. Harman International Industries, Incorporated

16. Infineon Technologies AG

17. Magna International, Inc.

18. Panasonic Corporation

19. Robert Bosch GmbH

20. Valeo S.A.

21. Visteon Corporation

22. ZF Friedrichshafen AG

23. Other key players

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/connected-car-devices-market/1287/

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656